For a quarter of a century, consumer technology was the most dependable disinflationary force in the world economy. Each year, the device in the hand did more and cost less, and that quiet subtraction flattered every inflation print on earth. That era is over. This is slowly turning into consensus, with the "technology is always deflationary" crowd finally yielding to the weight of evidence. We have chronicled the long, cascading narrative of this Silicon Shock since its first tremors. The structural phenomenon we originally christened as techflation has since hardened into the invisible gravity of the global macroeconomic landscape. It has broken out of its cage; today, it is actively distorting core monetary gauges, bending both producer prices and personal consumption expenditures into its own inescapable orbit.

It is a profound inversion. Technology has never been considered a source of inflationary pressure. Even in recent years, when the cost of living became a persistent concern, blame was heaped on traditional causes: tariffs, then energy, then labor. Each had a face the public could resent and a politician willing to point. But those costumes have worn through. The trade fights have cooled, and oil has come off its war-driven highs as the market begins to look past energy as the whole story. With the usual suspects fading from the conversation, the eye naturally travels to the one category that was never supposed to climb at all.

The world is now busy inventing names for it. Some are settling on chip inflation; others have reached for memflation or ramageddon. The vocabulary is the tell. One does not coin a word for a phenomenon one intends to forgive. A villain is being assembled, and the naming is the first stage of the assembly.

The evidence has stopped being anecdotal. We use U.S. numbers to make the point, but the forces are global. Headline inflation in the U.S. has climbed to 4.1%, a three-year high and the fourth straight month of acceleration, with the core measure lodged at 3.4% and no longer falling toward its target. Producer prices for electronic components have run up close to 27% over the past year, from under 6% in January; computer software and accessories on the shelf are up around 15%; and in the channel, contract prices for ordinary memory have more than doubled in just two quarters. By one estimate, the data center build-out alone is now adding roughly 0.4 points to core inflation. This may not appear dramatic, but it is an extraordinary share to assign to a single technology.

The institutions that move slowest have begun to concede it. The Federal Reserve now acknowledges that the construction frenzy is probably pushing inflation higher, and one of its governors has warned of a fresh price shock driven by AI investment demand. The question that its own economists pose is the one that should trouble the memory makers most: whether this is the old, volatile chip cycle, soon to turn, or a new supercycle that will not.

As always, we are staggered by how much the market believes it can explain away through exhausted phrases like "cycle" and "supercycle." But what separates this wave from its predecessors is that it answers to no embargo and no statute. It is pure arithmetic. A boom in one corner of computing is consuming the parts every other corner is built from. Agentic systems that run without pause and a token economy without a ceiling pull memory into the data center, leaving the rest of the world to bid for the remainder. This is the flip we described: pricing power migrating from the cutting edge to even mature products because of capacity reallocation. Producers who spent two decades competing with one another into losses now dictate terms, carrying the composure of a supplier who knows the buyer has nowhere else to go.

In the hunt for a villain, simplicity wins, and it will not matter whether the simplest story on offer is the right one. Globally, the prices of everyday technology products have begun rising like never before. The headlines are turning shrill; consumer gadgets are no longer luxury items, and rising prices hurt the most vulnerable sections of the economy. Those implementing the sticker price shocks have a simple defense: they are helpless because their component costs, particularly the easily understood memory chips, are skyrocketing.

That memory makers are posting extraordinary profits does not help. In financial markets, the vast majority cannot reconcile the fact that companies they have historically held in little regard are suddenly making more money than their favorites in other sectors. With new narratives being actively supplied by popular gadget makers, chatter about "price gouging" is rising in volume.

The account is skin-deep, but it lands on a target the world was already primed to dislike. The memory makers resented long before they were rich, largely dismissed as commodity peddlers. Now, the fattest margins in their history arrive to harden the grudge rather than soften it. Unless they put in real effort to rewrite this story, and with the minor exception of Micron, nothing suggests they intend to, this does not remain a quarrel about laptops. It worsens in ways they are not braced for, and its next stage is geopolitical.

Everyone's Favorite Hate Object

We were not surprised when Apple's outgoing chief blamed memory, and not foundry costs or anything else, for the prices it was lately forced to raise. Memory is the safest thing to accuse in the supply chain. No one boycotts a chip they have never seen, sold by a company they may not be able to name, and these particular companies are the easiest in technology to resent. Their margins have climbed to brush Nvidia's, and a component supplier earning like the most glamorous name in the industry draws every species of scorn, snideness, and envy the market keeps in stock.

The resentment is not confined to angry consumers. It runs up the chain to the makers' own peers. At its June shareholder meeting, TSMC's chief told the room he envied memory's 80% gross margins but would never reach for them, drawing a careful line between his disciplined foundry and the opportunists down the road. In the same month, TSMC quietly informed customers of price increases across nearly three-quarters of its wafer business. The point is not that TSMC is a hypocrite. It is that memory that has become the foil against which everyone else, even a fellow monopolist raising its own prices, gets to look restrained.

The analysts who do not cover memory pile on from the other direction. To them the unbelievable margins are not evidence of a structural shift but proof that the top is near, a cyclical reckoning overdue, never mind that almost none of them forecast even a sliver of the run that multiplied memory prices severalfold, and in places far more. Having missed the climb, they are determined to be early on the fall.

What makes memory such a comfortable target is partly that few credit the makers with doing anything extraordinary. But it is more than the makers, the Korean two above all, simply take it. They absorb the blame, the scorn, and the cyclical obituaries without rebuttal, and when they do surface in public, they wear the humility face, all but agreeing that this strange golden phase will pass and normal service resume. It will not, at least not soon, and not only because of demand and supply. The difficulty of adding capacity, and of anyone outside the three even attempting it, is something we have set out at length (Is DRAM at a Permanently Higher Plateau?). In that world, the studied modesty is not grace. It is an invitation. A producer who will not make his own case hands it to everyone who would rather make it against him. The memory makers have explained the cycle a hundred times. They have not begun to explain themselves.

There Has Never Been Any Respect for Memory Makers

Try a question that sounds absurd and is not. When did the world last treat a memory chief as an oracle of the AI age, the way it hangs on every word from Jensen Huang, or settle in for an hour to hear his view of where it is all heading? When did one of them command a stage as a visionary rather than a supplier? It does not happen. Micron's boss was at last year's celebrated White House tech dinner and has stood with the administration to pledge American investment; the two Korean chiefs shared a podium with their own president just this week. But notice what those appearances were: a number pledged, a fab promised, a national champion taking its assigned place. No one asks the memory makers what they think the future holds. It is quietly assumed they have nothing worth hearing.

Three years into the generative AI era, a grudging consensus has formed that the cognitive layers are no longer untouchable. Software development, the purest office work of the industry, has lost its old unquestioned scarcity; the argument was resisted at first and is now nearly conventional. Yet as software sheds its halo, the reverence only migrates one rung down, to chip design. We argued in January that design is hardware's software, the high-status intellectual labor the market knows how to admire, abstract, and architectural, and apparently weightless (Chip Design: Hardware's Software). Even as the crowd around it thickens, Arm, Qualcomm, and a steady parade of Chinese entrants, the romance of cognition clings to it. Foundry work keeps its honor, too. The world has learned, at least dimly, to treat the yield and packaging of a TSMC as a kind of miracle.

Memory was never extended the courtesy. To investors, it was a cycle, to customers a cost line, to technologists a commodity. The shorthand was self-satisfied: a chip is a chip, standardized by committee, so where is the genius? Memory has design, but not of any complexity or intricacy that anyone needs to admire.

Memory's hardest problems sit precisely where the market refuses to look, in the etching of capacitor structures at brutal aspect ratios, in deposition, in yield, in coaxing billions of identical cells to behave almost perfectly. It is why the masters of logic manufacturing, Intel and TSMC among them, do not simply wander into leading-edge DRAM or HBM and win. The cleanest proof arrived this year from inside the industry's own leader. Samsung, the rare house that builds world-class logic and memory under one roof, stumbled on the yields for its most advanced AI memory and watched a pure-play rival take the crown. Mastery here is not bought with a balance sheet or borrowed from an adjacent triumph.

None of which the world credits, and that is the danger, not the insult. Respect would have bought them defenders, the customers, analysts, and commentators who explain a company charitably when its prices turn. The danger in that is not wounded pride. These are engineers, and they may be perfectly content to be unglamorous. The danger is subtler and worse: disrespect, sustained for decades, has left them without a single friend. So now, at the precise moment the world goes looking for someone to blame, the memory makers find themselves the most profitable companies on earth and with nobody in their corner.

Geography of the Grudge

The second root is harder to say without being misheard, so we will say it plainly. The two largest memory makers are not American. They are Korean. To a macro commentator in the West, that single fact is quietly doing a great deal of work.

The argument writes itself on the podcasts and the cable hits. Several of the largest American companies have begun to lag the broader market, their margins visibly pressed, and the cause is increasingly placed offshore. For the multitude raised on passive investing, who watched their funds compound on the long outperformance of the majors, the Mag Seven and every moniker before it, a foreign supplier eclipsing those names can only be temporary, a glitch their corporate chieftains, and if not them then their politicians, must correct.

Of late the story has turned further. On consensus forecasts, the three memory makers may earn more in operating profit next year than Apple, Meta, Alphabet and Amazon make between them, with enough left over for a TSMC or a JP Morgan, if not both. A component supplier, out-earning the marquee American names whose products it sits inside. Set that way, it reads as an injustice in search of an author. One has only to read the popular commentators in the financial press to feel the frustration: companies that merely live on the largesse of the giants, on their capex, are making this kind of money, and seemingly at the expense of the very portfolios built on those giants.

There is an unspoken assumption beneath it, that a domestic champion should be shielded from the shock, and that the foreign supplier exists to absorb the pain. The notion that the American giant might instead take the hit itself, accept thin returns or a stretch of losses to spare its customers, is treated as faintly unthinkable, while the identical sacrifice is demanded of the foreigner without a second thought. If only those firms would charge less, the reasoning runs, the shelf would be cheap again.

The history beneath this is badly told. In the Western version, the downstream American giants built the Asian fabs; Apple, the story goes, made TSMC. As we set out in our ASML piece, the corridors of those fabs remember it differently. For years the manufacturers held almost no pricing power, their margins kept on a tight, Cupertino-controlled leash by the very clients who used rock-bottom components to flatter their own returns (The Last Polite Monopolist). Micron, the lone Western maker, has begun, gently, to say as much, noting that the aggressive squeezing of the last downturn is what starved the investment and seeded today's shortage. It is a fair point and a useless one. It explains the system to a room of investors. It does nothing to soften a household paying more for a laptop.

The fabs feel no debt to the clients who spent a decade crushing them, and no urge to subsidize the downstream any longer. As the bill reaches the ordinary consumer, the distance between the Western assumption of cheap components and the Asian refusal to keep providing them stops being a supply dispute. It becomes a grievance with a flag on it, the raw material from which the next stage, the geopolitical one, is built.

One aside, since it returns when we close. Memory is among the few frontier technologies where the West seems strangely relaxed about Chinese parity. With prices spiking, Apple is already lobbying Washington to loosen the curbs on sourcing from a blacklisted Chinese maker, the case being that Chinese gains in memory threaten far less than they would in models, foundries or EUV. It is a small crack in a wall the West built on purpose, and where small cracks lead is the subject we end on.

A Trillion-Dollar Industry Cannot Whisper

The memory makers have outgrown their own language, and they have not noticed. For decades, they spoke exclusively in the impoverished grammar of the "cycle." Demand was strong or weak, inventory high or low, price down then up then down again. Every presentation relied on the same spartan vocabulary to explain their helpless, almost compulsive behavior around CapEx.

When the AI boom broke their historical trendlines last year, their language did not evolve; it just bolted on a prefix. Now, everything is a "supercycle." The makers, particularly the Koreans, seem entirely content to cosplay as the inadvertent, passive beneficiaries of a weather event. That studied humility might have suited a commodity price-taker in 2015. But for a cohort of companies now collectively commanding trillion-dollar valuations and gatekeeping the most critical constraint of the AI economy, this silence creates a dangerously wrong impression. It is an elementary error of public relations, and it is actively mutating into a legal liability.

Retire the 'Supercycle' Before It Becomes Exhibit A

Five days ago, the cost of that silence materialized in the U.S. District Court for the Northern District of California as Garciaguirre v. Samsung Electronics. The 17 plaintiffs—a mix of individuals and small businesses—claim the memory oligopoly conspired to keep commodity DRAM artificially scarce to inflate prices. The complaint argues the makers used their coordinated pivot toward High Bandwidth Memory (HBM) as a smokescreen to deliberately throttle the production of older DDR3 and DDR4 modules.

This is exactly what happens when you refuse to explain yourself. Extraordinary margins attract extraordinary scrutiny. If the Korean giants refuse to publicly articulate that their chips are not simple commodities, but rather bespoke, thermodynamically complex engineering marvels critical to global security, they will be treated exactly like a cartel. The public will demand they charge less, regulators will demand they pay more in fines, and politicians demand they pay more taxes.

People like GenInnov should not be the tiny group to explain why these companies are critical for the security and primacy for those intend to lead the AI industry or their products are as customized as GPUs of NVIDIAs or AMDs. If the three companies do not want to be banded together as a world’s macro-hurting cartel, they must take charge in retiring the explanations revolving around “super-cycles,” often initiated by their own managers and never resisted in conversations involving analysts and other pundits.

The story they decline to tell is the most interesting one in technology. Compute has grown heavier at every layer, from the components on a single board to the architecture of an entire AI factory, and the demand has rippled vertically through everything that feeds it, from MLCCs and substrates to the lasers and PCBs of optical transceivers, where lead times have stretched from weeks to months. Memory caught the largest wave of all. The models themselves have grown denser, and the regurgitation that began with reasoning and is compounding in the agentic era consumes memory faster than almost anything else, because a machine that thinks longer and never stops must hold more of its context in silicon. Nvidia spells this out in public: as context lengths grow and inference turns interactive, memory becomes the dominant constraint on efficiency. Its newest accelerators carry hundreds of gigabytes of HBM each, several times the prior generation. An AI server now holds eight to ten times the memory of an ordinary one, and HBM burns roughly three wafers for every one a commodity part would need. The data center has climbed from a third of DRAM demand to half, on its way to two-thirds. That is why the shock spread outward from HBM into DRAM, into NAND, and finally onto the shelf.

That last point matters. The lawsuit may fail. It may deserve to fail. Parallel investment in HBM is not proof of collusion; it may simply be what happens when every serious AI customer bangs on the same three doors at the same time. But the lawsuit is still important because it shows the shape of the accusation now forming. The plaintiffs do not need to understand HBM yields, TSVs, wafer starts, packaging constraints, Nvidia roadmaps or hyperscaler contracts to create a story. They need only four words: they all moved together.

That is why “supercycle” is no longer harmless. It sounds like a shrug. It sounds like management saying prices rose because prices rose. In a commodity downturn, that language merely annoys shareholders. In an inflationary boom, with laptop, console and phone prices rising downstream, it becomes an exhibit.

The C-suites in Seoul might loathe the podcast circuit, and they may lack the theatrical flair of the American tech majors, but remaining aloof is no longer a luxury they can afford. An industry with three trillion-dollar companies cannot outsource its narrative to its customers and its critics. The industry is now too large, too profitable and too politically exposed to hide behind commodity diction. If Samsung, SK hynix and Micron want the world to understand that this is not a cartel story, they must stop speaking as if price is an act of God. They need to show the order books, the capacity math, the fab lead times, the HBM trade-offs, the customer commitments, the packaging bottlenecks and the economics of underinvestment after the last bust.

Until the makers say it themselves, in words larger than supercycle, they remain what they have always allowed the world to call them: passive beneficiaries in the boom, and in the bust the simpletons who never saw it coming. The error compounds the moment anyone bothers to look, as being shown by the plaintiffs of the lawsuit.

When the Stock Becomes the Story

The second error is one of stewardship, and it is becoming the most expensive.

These are no longer specialist chips followed by a narrow circle. SK Hynix briefly overtook Samsung to become the most valuable listed company in Korea, worth about $1.35 trillion; Micron crossed a trillion dollars in value for the first time this spring. They are among the largest single expressions of the AI trade anywhere. And their home market cannot carry them safely. Samsung and SK Hynix together now make up more than half the entire KOSPI, up from a third a year ago. When two stocks are the index, the index has nowhere to hide.

So it did not hide. After Korea launched sixteen single-stock leveraged ETFs on the two names in late May, retail money poured in, the funds swelling past $9 billion with roughly nine in ten holders being individuals. The world’s most volatile market turned more volatile with these products. A week ago and a day after the regulator admitted it had approved those products too hastily, the whole thing broke. The KOSPI fell 9.99%, with Samsung and Hynix having their worst single day since the 2008 crisis. The leveraged funds built on them fell roughly a quarter in a session. This is what a casino looks like when the house steps away from the microphone.

The memorymakers did not build those products and cannot control their stocks, and they should not try. But that is not the obligation. The obligation is to stop feeding a vacuum. A company of this size and volatility has to communicate through the turbulence, narrow the informational gaps, explain capacity and demand visibility and downside risk, and warn plainly against speculative excess rather than bask in it. Silence or even practiced humility is not neutrality here. When the leverage finally unwinds and retail investors are wiped out, the firms that said nothing, that behaved like quiet engineering houses while a bubble inflated on top of them, will be the ones blamed for the wreckage. That too is an elementary error, and the scrutiny that punishes it is rising by the week.

Do Not Invite the Cartel Story

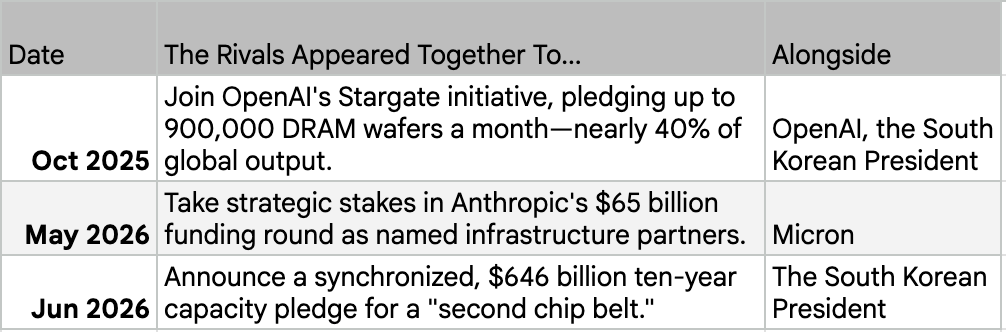

Two audiences appear to have read our recent notes with unusual care, and we find we are not flattered. The first are the plaintiffs. For much of last year we pointed, more or less alone, at the oddest tell in the industry, three ferocious rivals retiring DDR4 in near-unison, a coordination we called unprecedented at the time and of historic significance later. That single observation is now the spine of a federal lawsuit discussed above. The second reader is the Korean state, which seems to have taken to heart our more sardonic line, that the surest way to prove these blood-feuding rivals were not built solely to ruin one another would be to line them up behind their president. On Monday, that is exactly what happened. For once, we would rather not have been read so closely.

The third error is the most dangerous of the three, because it needs no truth to do its damage, and this week it walked onstage in person. To a domestic audience, this is excellent political theater; it is the visual of national champions securing the semiconductor frontier. But to a global economy choking on techflation, it is catastrophic optics. Seen from a world wincing at its memory bills, the same frame reads differently, the two firms that make two-thirds of the planet's memory holding hands with their president for the cameras and promising, in unison, to steer the supply for ten years.

As such, the companies that claim to be fiercely independent competitors, the pattern of joint appearances is starting to jangle.

Each tableau, two rivals controlling 70% of DRAM and 80% of HBM, a head of state, a decade of synchronized capacity, reads less like national champions than like a cartel taking a podium. The viral fried-chicken dinners that turned Korea's chip and tech chiefs into folk heroes beside Nvidia's Jensen Huang only deepen the sense of a small circle perpetually in one another's company. None of it proves anything. Much of it is simply what national industrial strategy looks like now. But politics does not process nuance. Angry consumers see dearer gadgets, device makers point upstream, analysts see record margins, and lawyers see concentration. The old word assembles itself: cartel.

The memory makers have a record they seem to have forgotten. Between 1998 and 2002, the industry ran a convicted price-fixing conspiracy. Executives went to prison, and hundreds of millions in fines were paid. The named victims included Apple, the very same firm pointing fingers today.

This is the same elementary error in its most combustible form. Compete in public and be dismissed as simpletons; appear in concert and be suspected as conspirators. The only exit is to explain, separately and clearly, that disciplined capacity is a response to demand and the brutal arithmetic of fabs, not a private agreement, and to say it before a regulator or a candidate says something more convenient first.

Speak, or Be Spoken For

Micron cannot carry the industry's case forever. The lone Western maker has begun, gently, to make it, arguing that years of brutal customer pricing starved the investment that would have prevented today's shortage. But Micron is the smallest of the three and the most conflicted witness, a beneficiary defending its own record margins. The two firms that actually set the weather, the Korean giants, say almost nothing in the languages that matter. That silence has stopped being safe, because the stakes have outgrown the pricing cycle.

Consider how critical memory has already become: Apple is currently lobbying Washington for permission to buy memory from CXMT, a Chinese maker blacklisted by the Pentagon. When the world’s most valuable company asks the U.S. government to trade a national security red line for component price relief, you know exactly how immense the pressure has become.

Meanwhile the relief everyone is counting on in the long-term may also not arrive. The tens of billions in new fabs from Samsung, SK Hynix and Micron will not produce at scale until 2028 or beyond, and on the present trajectory of AI memory demand, even that may fall short. Long before the concrete is poured, the inflation that memory is now feeding could do real damage to the very tech demand the boom depends on, a feedback loop we have warned about for some time.

And the mood is turning. The din against the memory makers is rising from every direction at once, from the product chieftains raising their own prices, from the podcasters, from the commentators. Inside seven days the memory makers were sued for conspiracy, watched their shares crater in a leveraged panic, and then, in the third act of the same week, lined up beside their head of state to pledge a decade of joint construction. Any one of them is survivable. Together they compose a portrait, and not a flattering one. Here is an industry earning margins higher than almost any company in history, and the world has decided the winners are accidental, the profits unearned, the beneficiaries undeserving. That resentment does not stay abstract. It hardens into lawsuits, into hearings, into trade fights, into the search for a foreign villain.

The makers do not need to perform at Jensen Huang's volume, touring the world with a roadmap and a leather jacket. But they do need to be heard, in the outlets ordinary people read, giving their own account of why scarcity exists and why discipline is not collusion. Until the largest two learn that, they are far more exposed than any product cycle would suggest, not because the demand is fragile, but because they have not learned the nuances required to manage being the most profitable companies on earth. And if they imagine the cure for their stock's wild swings is to ship the volatility abroad, an SK Hynix listing in New York into another thin pool of leverage, they are in for a surprise. They are already drawing the gaze of politicians in their own capital and well beyond it, and they have not begun to manage what people believe about them.

Forty years ago, memory was the quiet engine that made the digital world cheap. Today it is the upstream producer the world has chosen to blame for making it expensive, an OPEC that has not yet realized it is one. The barrels did not learn to speak in the 1970s, and the producers paid for it in politics for a generation. The memory makers can explain the AI shock now, in their own words, on their own terms. Or they can wait, and be explained, by the angriest audiences they have ever had.