Some Semi-good news for GenInnov Thoughts readers: Nilesh is on leave!…which means your inbox gets a rare chance to draw breath. You know how it works by now. A document lands. Before you have finished the first, a second arrives to open an entirely new front on innovation, usually around the point you were quietly hoping for a conclusion. We joke on the desk that Nilesh writes the way the HBM makers ship: continuously, at scale, and with a backlog that never clears. Each note is genuinely insightful, the sort of thing you set aside for a quiet Sunday and a strong coffee. But by the time you have worked your way through one, you need a second coffee, because another three or four land in your inbox. This note, however, comes from a different chair, and out of respect for every inbox Nilesh has stress-tested, it will try to make a single point and land it before he returns from leave and normal service resumes.

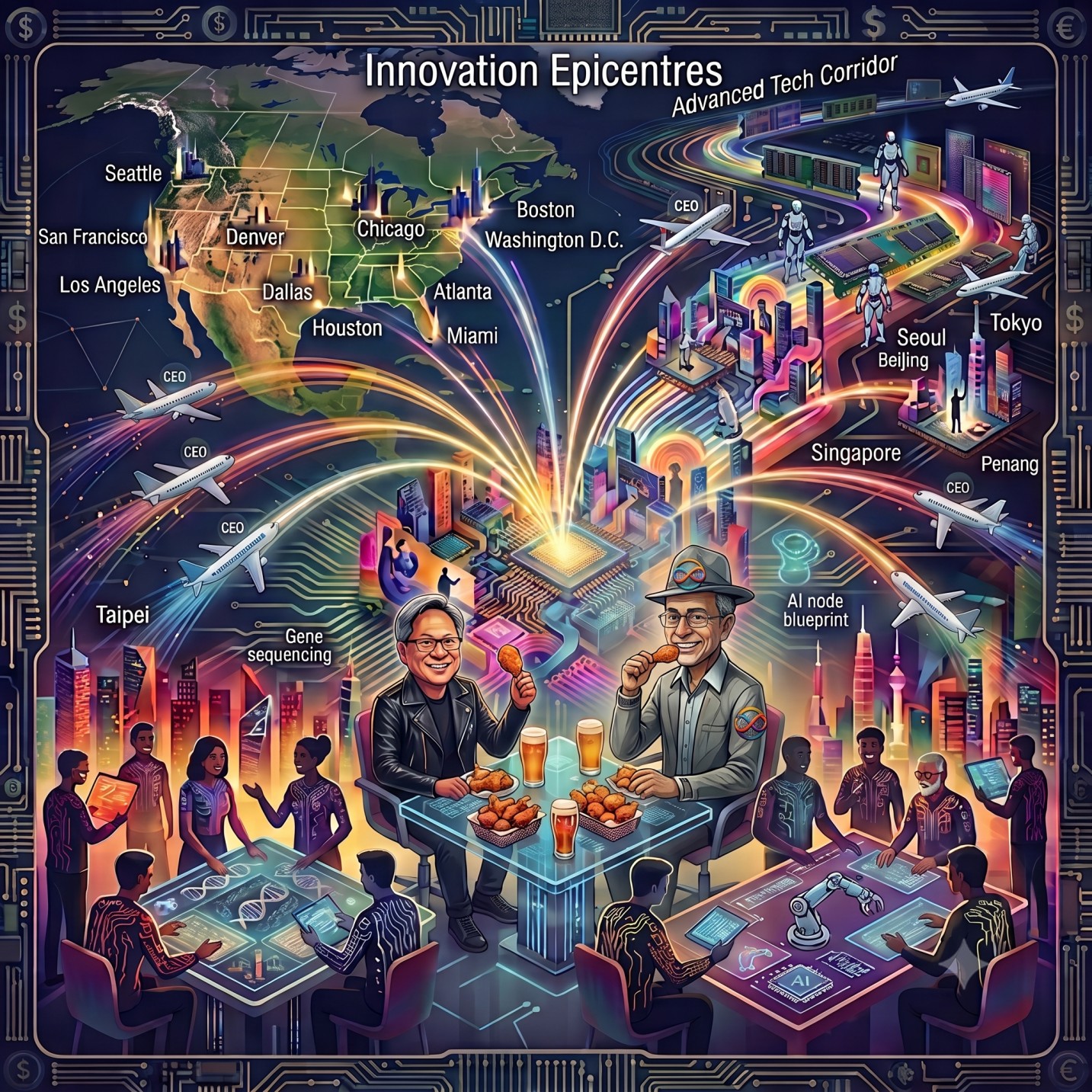

The point of this note, and there is only one, as promised, is what to make of a curious pattern: the world's most powerful technology CEOs flying east, again and again, to call on their Asian suppliers in person. It is worth asking what they have understood that the rest of us are still catching up to. The short version is that a handful of places in Asia have become genuinely irreplaceable, and that this has consequences reaching well beyond the chips themselves. Followed to its conclusion, it opens up an entirely new investing theme, one that leverages innovation in a very different way.

I. India has Bollywood, Korea has K-Pop, the US has Tech CEOs

America's most reliable cultural export this decade may turn out to be the celebrity chief executive. CEOs from the US are now making the pilgrimage to Asia with the regularity of a touring band, and drawing roughly the same crowds at the airport. Jensen Huang has reached the point where the black leather jacket is recognised before the man inside it, which is about as close to K-pop idol status as a sixty-something semiconductor executive is ever likely to get. Taiwan even has a word for it, Jensanity, coined in the same spirit as Jeremy Lin's Linsanity over a decade earlier.

Late May and into June saw the who's who of US tech CEOs pass through Asia. Lisa Su came through first. Jensen Huang touched down in Taipei and crossed to Seoul shortly afterwards. Intel's Lip-Bu Tan landed that same window. Inside a single short stretch, the AI era's most consequential Western executives, Huang, Su, Tan, Qualcomm's Cristiano Amon and Marvell's Matt Murphy, were all in the same city, taking closed-door meetings with the same set of supply partners.

Let us stop and consider for a second what is going on here. These are some of the busiest people on the planet, juggling their time between running multi-billion and trillion-dollar companies at the bleeding edge of a technology arms race, managing a sprawling set of stakeholders at home and abroad, and headlining one industry forum after another. These are not people with idle Tuesdays, and they guard their calendars the way TSMC guards a process recipe.

Yet within the space of a few weeks the same handful of them personally boarded planes, flew east, and committed capital in the billions across the semiconductor corridors of Asia. AMD alone announced more than US$10 billion in Taiwan ecosystem investment during Su's visit. That is a great deal of money to hand over in person when a wire transfer would have cleared before lunch.

II. Why Innovation Clusters are getting concentrated vs diversified.

The previous consensus view was that connectivity would dissolve geography. A gifted engineer anywhere, on the same internet, reading the same papers, wielding the same tools, ought to be as productive as one inside a cluster. Capital would chase talent wherever it sat. It was an elegant thesis.

Yet, it has turned out to be the other way around. Frontier innovation has grown more concentrated, not less, with clusters forming in a handful of specific geographies. The reason, as we see it, is that unlike in the world of software, the knowledge that matters most at this frontier does not travel down a fibre-optic cable. It lives in people. In the instinct an engineer develops for why a yield is quietly drifting. In the half-formed idea that becomes a product because two colleagues happened to share a lunch. In the method that walks out of one firm and into another inside someone's head when they change jobs. Economists call this tacit knowledge, and by definition it is the kind that cannot be written down well enough to send at distance.

ASML is the clean illustration. The company sits at the centre of a supply chain of some 5,000 firms, and the gravity of the operation keeps pulling talent and suppliers toward Veldhoven, a Dutch town most of the world could not find on a map and yet, it turns out, cannot manage without. This is not because the Netherlands holds any native edge in semiconductors, but because tacit knowledge, once concentrated, does not disperse. It compounds.

An innovation cluster, properly understood, is not a collection of factories. It is a collection of minds packed closely enough that knowledge keeps leaking across company lines whether anyone means it to or not. Past a certain density those collisions become constant, and the thing turns self-reinforcing in a way outsiders find almost impossible to break. The best people go where the best people already are, the hardest problems summon those who can solve them, and the gap with everywhere else widens every year. Unlocking where these Epicentres are forming leads us to new investment ideas.

Detroit was built this way, not by policy but by the gravitational pull of Ford, then GM, then every supplier and toolmaker and engineer who needed to be near where the cars were made. Bangalore did the same, compounding three decades of software capability until it became genuinely irreplaceable to every global IT firm regardless of headquarters. The cluster comes first. The wealth follows. Then, for a generation, the two feed each other in a loop that is very difficult to enter late.

In a similar way, modern Innovation Epicentres are forming across Korea, Taiwan, Singapore, Penang and some parts of Europe/US. The US executives making their pilgrimages have worked this out. The proof is no longer only in who shows up, but in where the largest technology companies are choosing to hire, build and embed for good. AWS has pledged around US$8.5 billion to Korean infrastructure by 2031, the largest greenfield foreign investment in the country's history. Google DeepMind signed an MOU to set up its first AI campus anywhere in the world in Seoul. Microsoft's Taiwan AI R&D centre has matured into a full development operation that keeps adding engineers. Micron broke ground on Singapore's first HBM advanced-packaging facility, a US$7 billion commitment that comes online this year. Intel's advanced-packaging complex in Penang is 99 percent complete, backed by US$2.5 billion.

These are the moves of companies that have concluded the knowledge they need lives in particular places and cannot be shipped home.

III. The Engineers, the Campuses, the Capital

So, back to the visits by the US CEOs. They are the visible surface of something deeper: an accumulation of human capital and institutional plumbing that has become self-sustaining in a way the earlier Asian manufacturing waves never were. Consumer electronics in the 1980s, PC assembly in the 1990s, those were extractive arrangements in which the intellectual property stayed elsewhere. The cluster executed; it did not originate. What is different now, and what makes the moment matter for investors, is that origination is increasingly happening inside the cluster itself.

It starts with the engineers, because capital rewards the people in the room where the IP is made. The average SK Hynix employee earned around 185 million won, close to US$130,000, in 2025, a record for the company and a jump of nearly 60 percent in a single year, and in a peak year the profit-sharing bonus alone can approach half a million dollars. A salary like that does something to a society, and to the answer a Korean mother gives at dinner when asked what her child does for a living. It bends an entire generation's ambition toward the frontier. When the highest-status, best-paid career in the country is not law or banking but memory architecture and AI systems engineering, you get a compounding dynamic that is very hard to reverse from outside.

You can watch the status shift play out in the oddest places. SK Hynix's plain company jacket, logo stitched on the chest, has become genuine status apparel in Korea, listed on second-hand sites this spring as the best blind-date look money can buy and parodied on SNL Korea as the garment that turns a sneering luxury-store clerk instantly courteous. Matchmakers now place chip engineers in the same bracket as doctors and lawyers, and apparently the running joke is that a Hynix employee claims to work at Samsung first and only confesses to Hynix once the date is going well. Taiwan has its own version of the same vanity: TSMC-branded shoes, modelled by chairman C.C. Wei at the company sports day, became a national talking point and now sell out as collectable, employee-only merchandise. When a chipmaker's logo carries this much cachet, you are no longer looking at a manufacturing job. You are looking at a new aristocracy.

The same story shows up wherever you look across the corridor: the talent, the infrastructure and the capital are all being committed in the same handful of places, as the table below sets out epicentre by epicentre.

IV. From the Innovation Epicentre to the Economy

What separates Korea and Taiwan from the earlier Asian manufacturing centres, and what makes Singapore and Penang the increasingly interesting next tier, is that the cluster has begun to organise itself. Manufacturing creates the engineers. The engineers create the knowledge density. The density creates the startups, and the startups create the next generation of firms, each layer funding and recruiting from the one beneath it.

This is the sequence that produces compound growth rather than the linear kind, the point at which a region stops executing other people's designs and starts generating its own companies, its own research, its own futures. Bangalore is the instructive parallel: for two decades an execution hub for Western software, until the knowledge density crossed a threshold, its engineers started their own companies and the city turned generative. Asia's AI corridor is earlier in that sequence. The sequence is the same.

What matters for the rest of the economy is that an innovation cluster of this size does not stay inside the factory gates. When the best-paid, highest-status career in a country becomes memory architecture or process engineering rather than law or banking, the money runs straight into the wider economy. Salaries on that scale are not left sitting in deposit accounts.

They buy apartments and underwrite mortgages, they fill restaurants and shopping districts, they pay for private schooling and wealth management, and they seed the next cohort of founders. The cluster manufactures a class of high earners, and that class quietly reshapes the property market, the consumer market and the financial-services market around it. This is the mechanism by which a chip boom turns into a consumption boom, and it is already showing up in the numbers.

Singapore's economy grew 6 percent year-on-year in the first quarter of 2026, led by electronics on the strength of sustained AI investment. The city produces around one tenth of the world's semiconductors and is deliberately pitching higher up the value chain, into advanced packaging, AI research and the financial plumbing of the technology economy, rather than competing on raw volume.

Penang's electronics sector contributes some US$10 billion to GDP and sustains more than 200,000 jobs across over a thousand companies, and the state's GDP per capita has climbed to roughly 50 percent above the national average, the third highest in Malaysia and on a steeper path than at any point in the past decade. Strip away the jargon and these are rising household incomes, busier malls, and fuller order books for property developers and private banks: a semiconductor statistic transmitting into an ordinary economic one.

The capital has worked out what it is sitting beside. Taiwan has put state money behind an AI build-out measured in the hundreds of billions and now hosts more than ten thousand startups; Korea's venture investment rebounded to US$10 billion in 2025, with the chaebol, Samsung, SK, Naver and Kakao, acting as an exit engine that recycles talent and money back into clusters like Pangyo. None of this is the signature of a manufacturing boom. It is the signature of an economy that has turned generative and is beginning to spend like one.

V. What the US Tech CEO pilgrimage is telling us.

Return to the pilgrimage of our US CEOs. The lazy reading is supply-chain management conducted at altitude, which is not wrong. It is simply not the whole of it. Lisa Su could have sent a deputy. Jensen Huang could have secured his wafer allocation by phone and had the Korean fried chicken delivered to Los Altos. Neither did. They flew east, in person, at the top of the house, and gathered their partners around them, because in this region the relationship is the most valuable asset and presence is the only currency that settles it. The chicken, like the trust, does not travel well.

These CEOs have taken the view that the most important economic geographies of the coming decade sit in Northeast and Southeast Asia, and they are acting on it with their single most irreplaceable resource, which is not their capital but their time. In essence they are telling us that these Innovation Epicentres have crossed the threshold of self-reinforcing density, becoming something even the world's most powerful companies cannot replicate, route around or substitute. They can only travel to it and pay their respects.

The obvious trade is already crowded: own the chips, the foundries, the memory. What the cluster dynamics suggest is that a second wave of consequence is forming in these Epicentres. When the highest-status career in Korea is memory architecture, the economy does not merely grow; it transforms. The engineers earning half a million at SK Hynix buy apartments, take out mortgages, spend in restaurants and seed the next cohort of startups.

The roughly US$8.5 billion AWS commitment in Korea hires construction crews, facilities managers and operations engineers long before it hires a single AI researcher. Nvidia's Constellation campus generates demand for everything from commercial property to corporate banking. Micron's Singapore facility, scaling toward 3,000 staff, will be among the highest-wage manufacturing workforces in Southeast Asia. Penang's boom has already lifted its GDP per capita to the third highest of any Malaysian state. Innovation capex is transmitting into household income, consumer confidence, financial-services demand and local enterprise formation at a pace the macro consensus has not begun to price. Detroit in 1920. Bangalore in 2005. Same mechanism, different map.

The pilgrims are a useful clue, not a map. By the time a chief executive is on the tarmac, the epicentre he has come to see is already obvious to everyone. The harder and more valuable work is the earlier question: identifying which places are becoming Innovation Epicentres, which ones are next, and how the wealth they throw off will spread into the property, the consumption and the companies of the economies around them. The jets confirm the thesis. They do not write it. The new theme this note promised at the outset is to map those epicentres ourselves and to invest around them, well before the next plane lands.