A Longer Piece Even By Our Standards

There are titles one should never write. "The End of History" is one. "Permanent Plateau" is another. As such, anything with the word "permanently" in it may belong on the same list, because the arrow of time tends to find such titles and use them for target practice. The phrase above, many discerning investors may have noted, is borrowed, and borrowed on purpose. Irving Fisher told the world that stocks had reached a permanently high plateau in October 1929, days before the plateau gave way. The line has been a punchline for almost a century, ignoring the nuances contained in the note, like what the case has been for the end of history title.

So let us say it plainly at the top. We have not gone bonkers. We do not believe memory prices or profits will rise forever. This industry, like every other, will have its severe winters, with some pointing as if nothing has changed. What we believe is narrower and stranger. It is likely the least-explored, most important subject matter in global innovation investment.

Consider what has happened and gone almost unremarked. A sector that the investment world has treated for forty years as the bottom of the technology barrel now contains three companies worth more than a trillion dollars each. Each is on course to earn over a hundred billion dollars in profits. At least two, perhaps all three, may out-earn every Mag7 company and TSMC within a year or two. And yet the memory makers are still discussed, and still priced, as though they have been lucky tenants in a house that belongs to someone else.

The old prejudice has taken new forms in recent months. In much of the investment world, making money out of memory is almost regarded infra dig. Few serious tech investors want to display top holdings with any memory names in the list. Analysts are forced to abandon price-to-book-based fair valuation methods given the historic range rupture, but any anchoring based on the PE is more arbitrary than anything seen in the tech analysis. These stocks’ PE range history is unusable. And no one has the courage to apply even high-teens multiples, let alone 20x or 30x multiples, normally applied to the lowest-quality technology names in other segments. Meanwhile, the skeptical veterans are waiting for any 20-30% correction to say aloud what they have been muttering under their breath: these commodity stocks will repeat history and retreat to some sub-1-2x PB before anyone can detect bubbles anywhere else.

To some degree, the disdain was earned, once. For decades, memory really was undifferentiated capacity sold to the lowest bidder, and the snobbery was simply an accurate reading of the economics. But whether the prejudice has outlived its cause or not requires an answer to the question whether memory companies are different from here on, or in other words whether they are at a permanently different, aka higher, plateau.

For a change, we can now read long reports on the memory price implications that run to dozens of pages. They still discuss almost everything except the memory companies themselves. They discuss the demand: hyperscaler capex, token growth, server units, the bit-demand curve. They discuss sustainability, circularity, the risk of a bubble. They have begun to discuss the implications for other technology companies and even macroeconomic factors. They discuss everything that might be happening outside the building. What they rarely discuss is the companies themselves, their management, their products, and what is changing inside them that is handing them so much power. The firms are treated as weather vanes, not as actors.

That assumption is the subject of this piece. If these companies remain without any control over their destinies, they are surely different from every toolmaker, packaging company, optical component supplier, or even passive component supplier, let alone a foundry, chip design company, or software/model-making company out there, irrespective of the money they make now. We think it is wrong, and we think it is wrong in ways that matter for whether the profits are a fluke or a fixture. This note will therefore run far longer than usual, because to take the industry seriously, on its own terms, requires answering a list of questions that the prevailing coverage almost never raises:

- Evidence of business decisions, rather than mere demand factors, that changed the technology world, and caused the destination of hundreds of billions of profit dollars

- The reduced commoditized nature of memory in recent years, and the difference between something that is a commodity versus something that is cyclical

- If the whole world can see this happening, why can no one walk in and take it, not TSMC, not Intel, not China in any foreseeable future

- Where the industry's old scaffolding of common standards is quietly coming apart, and what does that tell us?

- How far has customization travelled, and is a memory part you cannot unplug a historic departure or a footnote?

- The behavioral changes that the one-time gains have brought about, and why memory business decisions are no longer demand-side driven, with non-management layers within the companies and surrounding governments joining the decision-making

The questions sound aggressive. They are meant to. But they are asked in good faith, and the answers, as we will try to show, require everyone in investment decisions to take these companies more seriously than they have so far. We begin where the silence is loudest: with a decision, taken a year ago, that moved hundreds of billions of dollars and was met with a shrug.

The Decision Nobody Covered

A year ago, three companies took a decision that moved hundreds of billions of dollars, and the world produced roughly nothing to mark it.

Let us be precise about the nothing. No magazine cover. No congressional hearing into why the memory inside every phone, every laptop, and every server on earth abruptly cost several times what it had. No antitrust inquiry, which is itself remarkable, given that the same industry was dragged through the courts in the 2000s for far less. No keynote, no documentary, no breathless feature in the technology press, which can be relied upon to write four thousand words about a folding phone. Not even the analysts, whose entire function is to notice things, noticed this one in any way proportionate to its consequence. The single most lucrative and unplanned collective move in the modern history of the semiconductor industry happened in plain sight, and the coverage it generated would embarrass a mid-tier product launch.

What happened was this. Within a few weeks of one another, SK Hynix, Samsung, and Micron each moved to wind down DDR4, an older, profitable, high-volume product still sitting under a vast installed base of the world's computing, at a time when demand for it was perfectly healthy. They did not coordinate, or at least there is no evidence they did and no need to assume it. There was no meeting, no cartel, no quota, no smoke-filled room. Three rivals who the market insists cannot occupy the same building without starting a price war simply arrived, within a fortnight, at the same conclusion: stop feeding the commodity, move the wafers to where the money is.

The market that the textbooks describe should not be able to do this. A commodity industry is supposed to behave like a school of fish that has learned nothing, building into every boom and drowning in every bust, because each player fears that the capacity it declines to add a rival will add instead. That is the prisoner's dilemma that kept memory poor for forty years. And here were three prisoners, separately, declining to defect. Whatever you wish to call that, it is not the behavior of the dumb cyclical the consensus still prices.

The result arrived almost immediately, and it was enormous. DDR4, the part nobody was supposed to care about, ran up several times in price within months as the supply was throttled and the remaining buyers scrambled. The squeeze dragged the rest of the memory complex up with it, and a good deal of NAND and storage besides. The numbers at the company level then stopped resembling a cycle and started resembling a different industry altogether. If three memory companies are expected to make over USD300bn more compared to expectations in the next four quarters, that money is coming from everyone else, and no financial journal or policymaker is still trying to go back to the point where the earth shifted.

Why the indifference? Partly the old prejudice we have already named. One does not study the decisions of a business one has decided has no decisions to make. If memory is a weather vane, then the only thing worth forecasting is the wind, and the vane itself is beneath notice. Partly it is a category error so deep it has become invisible: the entire apparatus of memory analysis is built to measure demand, because for forty years demand was the only variable that moved, and supply was assumed to be a reflex rather than a choice. Hand that apparatus a supply-side decision of historic consequence and it does not misread it. It simply does not see it, because it has no instrument pointed in that direction.

And partly, one suspects, it is that the decision is genuinely inconvenient. To take it seriously is to concede that these companies have agency and that their managements make choices that move the world. That concession is expensive. It means the memory makers might have to be analyzed like real businesses with real strategies, valued on something other than a price-to-book floor. It is easier to call it a fluke and wait for the crash that vindicates the prejudice.

We were likely the only one to write about the decision when it happened, and we said at the year's end that it was the most consequential business decision in technology that year. We would possibly go one step higher now and call it a decision of unprecedented impact for the global corporate world and economy. Still, we could be jaundiced. Maybe the decision was a necessity or the memory prices may have moved regardless because of the memory wall and other demand factors. Time to perhaps look at this more fundamentally, about whether memory is still a “commodity.”

Was It Ever a Commodity, and Is It Still One?

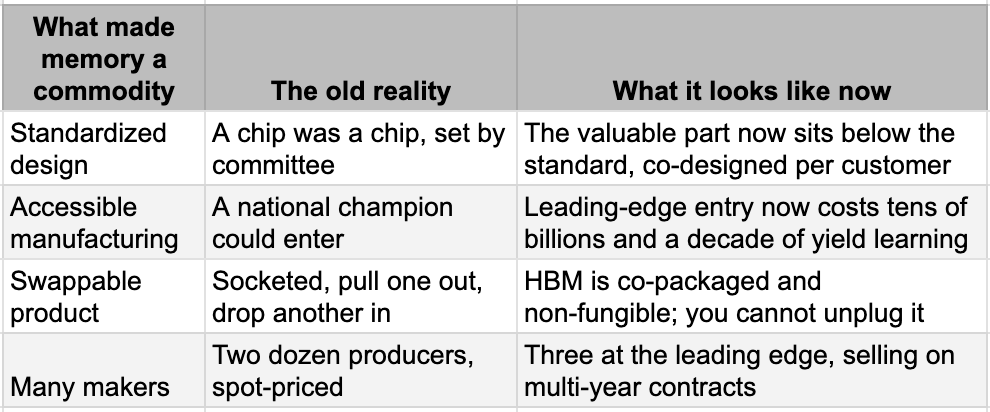

The word "commodity" gets used as a slur, which is precisely why it deserves a definition. A commodity is not simply something cheap, or something that crashes. It is something with a particular structure. It is swappable, one producer's unit interchangeable with another's. It is made by many, none large enough to set the price. Capacity can be added by anyone whenever returns rise above cost, so gluts are guaranteed. The producers are too numerous to discipline one another. And no brand, patent, or qualification gate lets any of them charge more than the next. Strip those five properties out, and you do not have a commodity, whatever else you have.

Notice what is not on that list: cyclicality. A commodity is usually cyclical, but cyclicality is not what makes it a commodity. Oil is violently cyclical, yet a barrel from a disciplined cartel is not priced like one from a thousand wildcatters. Luxury handbags are cyclical. Aircraft engines are cyclical. The cycle is a property of demand over time; commodity-ness is a property of structure. The two were welded together in the public mind by forty years of memory being both at once, until the industry's worst trait, its swings, became confused with its deepest one, its swappability. That confusion is the bears' entire case. "It always crashes" is a statement about the cycle. It says nothing about whether the thing is still a commodity. The two questions have come apart, and this is important before one determines how one values memory businesses.

Memory earned the label honestly. Four things made it the archetypal commodity. Its design was standardized by committee, so a chip was a chip. Its manufacturing, in the early decades, was within reach of any well-funded national champion. Its product was a socketed part, physically swappable, sold partly on a published spot price that read like a screen of pork-belly quotes. And there were dozens of makers. Put those together to get the business contemporaries called the "rice of the industry," a staple traded on volume, ruthlessly punishing anyone who produced it.

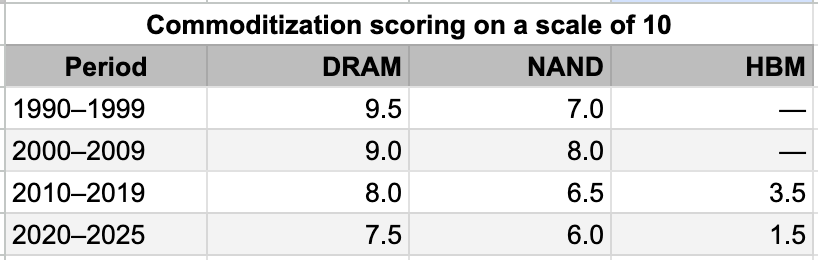

The honest way to track what has changed is to score it, even if arbitrarily to indicate the trends and to portray the current changed nature. The scale below runs from 10, a perfect commodity, to 0, a pure franchise. It measures the five structural properties, not the cycle, and crucially not consolidation, which is why a triopoly can still sell a high-scoring commodity.

The decades tell the story. The 1990s were as close to a pure commodity as electronics has produced: twenty-odd makers, a live spot market, perfect interchangeability. The 2000s deliver the most elegant proof of commodity-ness ever recorded, which is that the producers tried to escape it by crime. Facing prices below cost, the major makers ran a price-fixing conspiracy, and were caught, with criminal fines running past seven hundred million dollars in the United States alone. Cartels are usually read as evidence of monopoly power. In memory they are the opposite: evidence of an industry so structurally unable to hold a price that the only way to do it was illegally, and even then it failed. The 2010s are the decade everyone misreads. Elpida's 2012 bankruptcy left three makers holding more than 90% of DRAM, and the world concluded that the commodity had become an oligopoly. But the score barely moved, because the part did not change. A DDR4 module under a triopoly was still a swappable, spot-referenced, JEDEC-standard part. The industry consolidated. The product did not de-commoditize. Those are different things, and conflating them is the same error as conflating the cycle with the structure.

NAND ran a somewhat different path, which the table shows: it commoditized later and never as cleanly, then began climbing back down as the value moved into controllers and firmware rather than the raw die. We will come to why.

The break, when it finally came, came in one place and for one reason. HBM. Its score does not drift; it falls off a cliff, from a debut already below DDR to something close to a franchise. And the reason is the only thing on our five-property list that had never previously moved: swappability. For the first time, a memory part stopped being a thing you could pull out and replace with a rival's. Everything else, the consolidation, the capex, the discipline, made memory a better business. Only the death of swappability made it a different one.

So, was it ever a commodity? Yes, completely, and the disdain was once an accurate reading of the economics. Is it still? Less so every year, and at the frontier, no longer at all. And is it still cyclical? Almost certainly, yes. The winters will come. But a cyclical franchise that no one can enter and whose best product cannot be swapped is not the same asset as a commodity, even though both go up and down. The prejudice we opened with priced a commodity. The thing being priced has quietly become something else.

The Standard That Built the Commodity

If memory was a commodity because it was swappable, it is worth asking who made it swappable. The answer is a standards body most investors have never heard of, and its role is the key that unlocks the rest.

JEDEC writes the memory standards. It does so through a process designed, deliberately, to favor no one. Every member company gets one vote regardless of size. Passing a standard takes a two-thirds supermajority at committee and three-quarters at the board. Think about what a process like that can produce. A specification that requires a supermajority of competitors and customers to agree is, by construction, a lowest-common-denominator object. It standardizes the interface so completely that any vendor's part drops into any socket, which means buyers compete the vendors on price and nothing else. No single firm can bake its own advantage into the standard, because the standard needs its rivals' votes to pass.

That is not a flaw in JEDEC. It is the purpose. A standards body exists to make components interchangeable, which is to say it exists to commoditize them. For forty years the memory makers competed to build the most perfectly standardized possible product as cheaply as they could, and JEDEC was the machine that guaranteed the product stayed standard. The commodity curse was not bad luck. It was the system working as intended.

This yields the insight the rest of the piece turns on. Memory's commodity-ness was never really a property of the silicon. The cell inside a 1995 DRAM and a 2015 DRAM is the same idea. It was a property of the interface. Memory was a commodity because it was a socketed, standardized, swappable part, and the socket, not the silicon, is what JEDEC governed. Which has a sharp consequence. De-commoditization cannot happen through JEDEC, because anything that passes JEDEC is by definition something your rivals agreed to share. It can only happen by routing around the standard, by moving the value to a layer the committee does not reach. And that is exactly what has begun to happen.

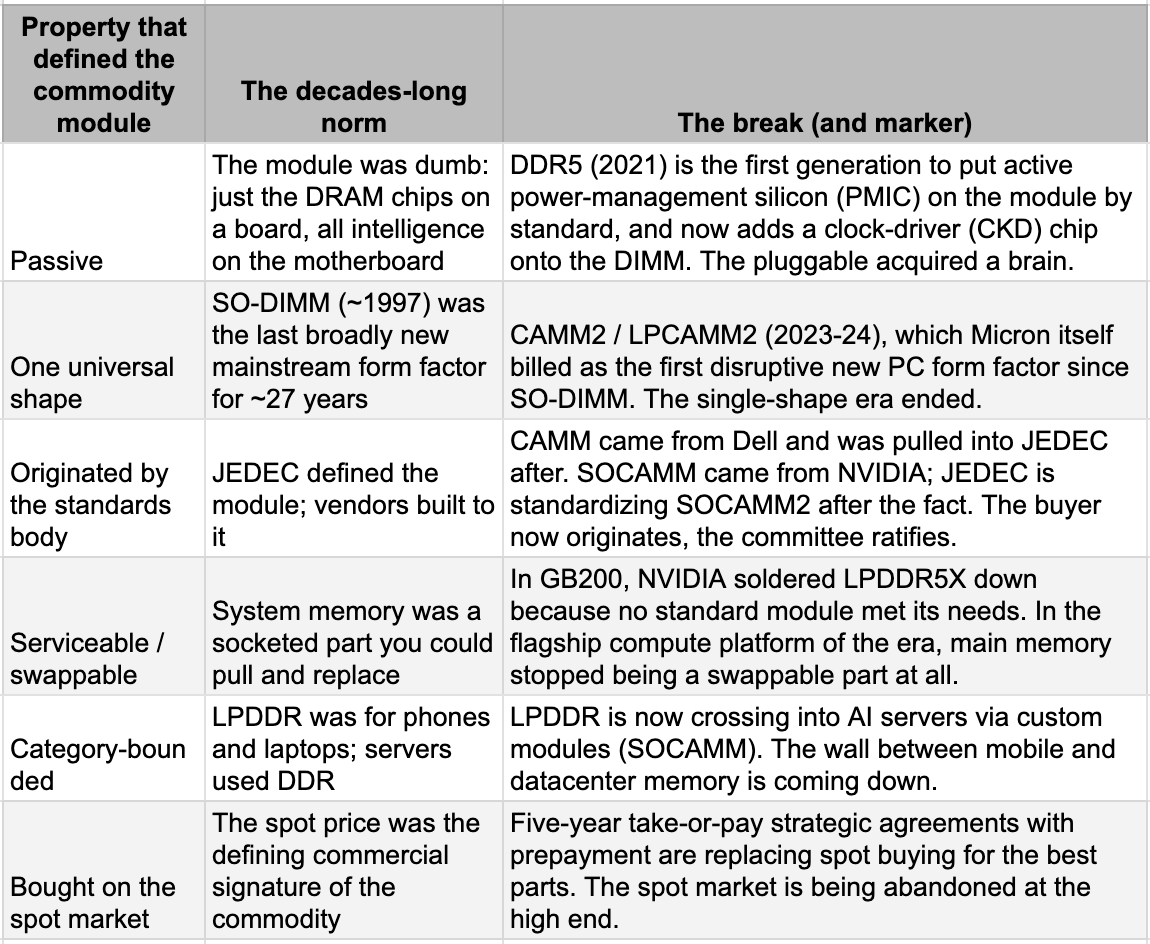

The Fraying and The Customization

The standard is not collapsing. JEDEC still meets, still votes, still ships specifications for DDR5 and its successors. What is happening is subtler and more important: the standard is increasingly governing only the layer that rivals are still willing to share, while the value migrates above and below it. It is fraying from both ends. There are three visible tears.

The first is that the value is leaving the standard from underneath. HBM still meets a JEDEC interface, a defined width, channel count, and speed envelope. But with the current generation, the base die, the logic layer at the bottom of the stack that does the real work, has moved off a memory process and onto an advanced logic node fabricated at a foundry, and it is increasingly customized to the specific accelerator it serves. The industry has a name for this, "custom HBM," and it means the same JEDEC-compliant stack is now a different physical product for an NVIDIA part than for an AMD part, and not identical between a Samsung stack and an SK Hynix stack even on the same chip.

The second tear is that the incumbents have learned to bend the standard itself. The cleanest example is mechanical. The HBM package-height limit sat at 720 microns through the prior generation. Meeting it for the taller new stacks would have forced the industry onto hybrid bonding, an expensive packaging step requiring new tools. So the limit was relaxed to 775 microns, and a further loosening toward 825-900 microns is now under discussion. The effect is to let the makers keep their existing tooling and postpone the costly transition, which conveniently protects the equipment they have already bought and the suppliers who sell it. A standard that flexes on request to defend incumbents' capital is no longer a neutral commoditizing referee. It is a lever, and the prominent incumbents have their hands on it.

The third tear is that new categories no longer wait for JEDEC at all. High Bandwidth Flash, the most plausible new memory tier on the horizon, is being standardized under the Open Compute Project, a hyperscaler body, by two of the four relevant makers, having started life as one firm's proprietary technology. SOCAMM, the memory module now going into AI servers, was defined by NVIDIA's requirements first and brought to the committee afterward. And NAND, tellingly, never had a single JEDEC interface to begin with: it split early into two rival camps, so the raw die was never cleanly swappable, and the value went straight into controllers and firmware. NAND did not de-commoditize by breaking a universal standard. It simply never had one, which is why its score in our table is lower and stickier than DRAM's. It is a preview of where the rest is heading.

The honest counter-current is CXL, a genuinely open fabric for pooling memory across a system, which pulls the other way, toward re-sharing capacity at a higher tier. It is the one place incentives still favor a real standard, because no hyperscaler wants a memory pool only one vendor can fill. So the fraying is not total, and we should not pretend it is. But the direction is unmistakable.

The module stopped being passive: DR5 moved power management (PMIC) and more control onto mainstream modules, so the module became less passive. The first new mainstream form factor in 27 years, and it didn't come from JEDEC, it came from a PC maker and then a chip buyer. The buyer now writes the module spec and the standards body follows, the reverse of the entire DIMM era. And the flagship server of the AI era ships with main memory that can't be unplugged. Any one of those is a departure; together they're a regime change in what a "memory part" even is.

The point is not that JEDEC is dying. It is that JEDEC is losing sovereignty over the layer where the money is made. Memory and storage are too important across the whole chain for every buyer and seller not to optimize or customize for specific needs within the AI hardware segments. The customization quotient is only going to rise in the coming years. Many see it clearly in SRAM, for instance, where the multiples far in excess of single-digit PE are never debated in private markets, but the trend is across the board, including in storage.

Why No One Can Build a Fourth, and Why the Market Still Misprices It

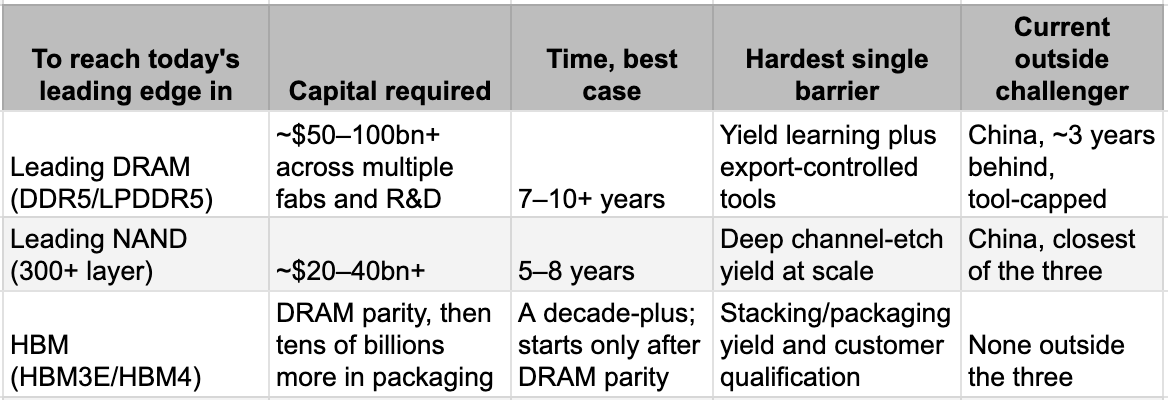

Consider a fact that should be impossible. The memory makers are now on course to earn multiples of what the world's leading logic foundry earns, the foundry the market rightly treats as the crown jewel of all semiconductors. If memory were the copyable commodity the consensus still assumes, that foundry, with its capital, its process mastery, and its packaging, would already be turning some of its lines to memory to capture those returns. It is not. Nor is anyone else. The capital required, while high, is available, the demand is visible and durable, the returns are extraordinary, and still no fourth maker appears. The reason is that the moat is not made of money.

The proof is the entity with the most money and the most reason to spend it. China has poured a decade and tens of billions of state dollars into the effort, and its leading DRAM maker is roughly three years behind the frontier, holding under five percent of the market against the incumbents' ninety-plus, and essentially absent in HBM. That is fast progress, but only at the commodity floor, not the edge. The best-funded attempt in history, freed from any need to earn a return, bought the cheap tier three years late. The binding constraint is not capital but accumulated knowledge: twenty years of yield learning, defect libraries, recipes co-developed with tool vendors, access to export-controlled equipment, and a thicket of cross-licensed patents without which it is not legal to ship a competitive part. Capital builds a fab in three years. It cannot build the two decades of process knowledge that make the fab yield, and a fab that does not yield converts billions into scrap.

The decisive evidence sits inside the club. Samsung has unlimited capital and its own leading foundry, yet in the current HBM generation it fell roughly eighteen months behind SK Hynix, failing one customer's qualification while a rival passed. If an incumbent with every resource can fall a year and a half behind on a single product, the barrier is plainly know-how, not money. And the point holds with even greater force for the logic foundries the market assumes could enter at will. They cannot, not for want of capital or management bandwidth, but because the processes optimize for opposite things. The deep charge-storage capacitor at the heart of every DRAM cell requires high-temperature fabrication steps that would destroy the low-thermal-budget transistors a logic process is built to protect. The two are opposite optimizations, not adjacent ones, and bridging them takes a separate decade of yield learning, not spare capital.

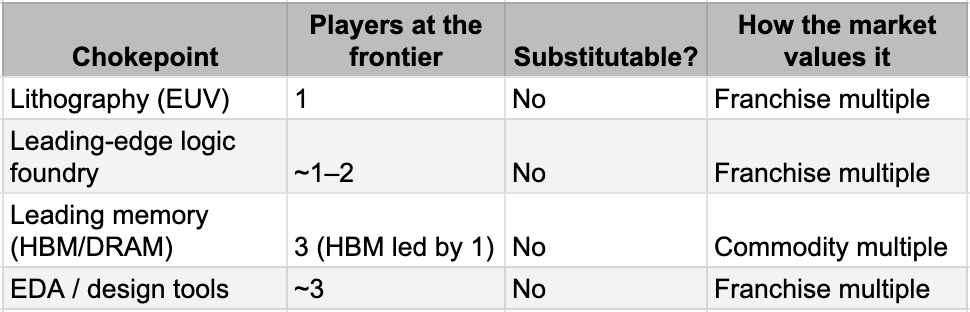

Memory, and by extension storage, is the only chokepoint of immense criticality that the market still refuses to price as one. The lithography monopoly trades on a franchise multiple. The leading foundry trades on a franchise multiple. Both are understood, correctly, as irreplaceable, and both are valued accordingly. The memory three are every bit as irreplaceable, by the entire argument of the last two sections, and a great deal more profitable right now, yet they are still valued many would not agree to value cotton or coffee producers, let alone on multiples that would embarrass the lowest-quality name in any other corner of technology. That is the anomaly. Not that memory may remain the biggest chokepoint, but that it is the one critical chokepoint the market has not yet admitted is a chokepoint at all.

What the Money Taught Them

Suppose the bears are right about the cycle. Suppose the winter comes, prices fall, and the extraordinary profits of this period prove one-time. Even then, something has changed that does not reverse, because the windfall has taught a lesson, and the lesson outlives the windfall.

For forty years these companies competed on volume and share, building into every boom because each feared the capacity it declined to add a rival would add instead. They behaved, in other words, as though they had no power over their own prices, because for most of that history they did not. What the past two years have shown them, in the plainest possible terms, is the size of the prize on the other side of restraint. They have watched what happens when supply is disciplined into rising demand: not a better quarter, but a reordering of where the profit in the entire technology chain comes to rest. That is not a fact a management forgets. It is the kind of recognition that, once arrived at, changes conduct permanently, in the way that any party which discovers it has been holding a genuine instrument of leverage, long suspected but never quite tested, tends to reach for it again once it has felt the thing work. Leverage that has been used successfully once is rarely retired. It is rationed, perhaps, and deployed with more care the next time, but it does not get forgotten, and it does not go back in the drawer.

What makes this durable is not a single management's memory but the breadth of who now shares the lesson. Tens of thousands of employees across the three firms have seen their fortunes turn on discipline rather than on the old race for share. A generation of executives has learned what chasing volume cost and what declining to chase it paid. And in the case of the two Korean makers, an entire national economy has felt the benefit, because when two of your three global champions stop fighting each other into the ground, the gains accrue not only to the companies but to the exchange, the tax base, and the trade balance of the country that houses them. That last point matters most, because it converts a corporate lesson into a national interest. The discipline now has a sovereign stakeholder.

This is where the behavior stops resembling a strategy and starts resembling the political economy of a resource state. Where a commodity's profit becomes load-bearing for a nation's accounts, the question of how hard to compete stops being a private commercial choice and becomes a matter of public welfare. The next time prices soften, the conversation will not be confined to a boardroom deciding whether to fight for share. It will reach the level at which countries ask whether the weakness is genuinely beyond anyone's control, or whether something might be done about it. Expect a Korean President to force Samsung Electronics and SK Hynix management to sit in a room to deliberate in the coming years if faced with sharply declining profits at these companies, which will also mean sharply reversing macroeconomic indicators.

To be clear, there is no cartel here, no agreement, nothing to prosecute. The discipline is overdetermined by a thousand private interests that happen to point the same way: the employee protecting a bonus, the executive who remembers the cost of the old reflex, the official watching the export line. Each acts alone, on a lesson they all learned at once. That is what makes it both legal and far more durable than any arrangement that could be written down.

A Different Plateau

We borrowed a discredited phrase for the title, and it is time to say what we actually mean by it.

We do not mean that prices will not fall. They will. We do not mean the cycle is dead. It is not. Memory will not only have its winters, but it will have fierce market share wars, new players, innovations that displace today’s products, and everything else one expects in every technology sub-segment.

Our argument is simple: the sector deserves more respect as another normal, cyclical, high-innovation segment. The market is slowly moving away from pricing it as in the days of yore: escapable, swappable, due for its comeuppance, valued against a book floor and a folk memory of crashes. Yet, for most, this is still only a trade; definitely not deserving of the same respect as the leaders of any other tech segments. We expect that to change only when the industry is analyzed more for what it is than just what happens around it.