A Strange and Unified Silence

In recent weeks, the semiconductor industry experienced a notable event. SK Hynix, Samsung, and Micron, the three titans of the memory chip industry, made a series of nearly simultaneous announcements. Each company declared it was halting new orders for DDR4, a workhorse memory chip that still powered vast swathes of the world’s digital infrastructure. On the surface, this was a straightforward product transition. In reality, it was a stunning break from decades of industry practice.

These companies are not friends. Their history is one of brutal price wars, intellectual property disputes, and a constant struggle for technological supremacy for the tiniest gains in market share. For them to act in such a coordinated fashion is unprecedented. It is as if Ford, General Motors, and Toyota all announced that they would stop making gasoline engines within a month, while millions of people still needed to fill their tanks.

This move was not a gentle phase-out. Previous transitions, like the shift from DDR2 to DDR3, were slow, gradual affairs. Manufacturers would support the older technology for years, allowing the market to migrate at its own pace. The DDR4 exit is different. It is an abrupt, forced march. The DRAM oligopoly effectively turned off the supply spigot while demand was still robust.

This coordinated action is a flex of collective market power that shows the memory industry is no longer playing by the old rules. The decision is driven by a powerful incentive to escape the unprofitable past and race toward a far more lucrative future. To understand why, one must first understand the curse that has haunted this industry for years.

The Commodity Curse of the Most Undervalued Segment in Semi

Memory chips are a marvel. They are the essential working storage for every computing task. And yet, they have long been treated like grains of rice in the semiconductor feast, perpetually presumed abundant and interchangeable.

For decades, memory chip makers have been shackled by the "commodity" label. This tag has been a source of immense frustration for the industry and its investors. While these companies produce some of the most complex and capital-intensive products on earth, they have rarely enjoyed the respect or the rich valuations afforded to all other semiconductor segments.

The reasons for this are rooted in the industry’s history. The memory market was once a crowded field, with dozens of companies vying for business. This led to savage, cyclical price wars. When demand was high, companies would invest billions in new fabrication plants. But this new capacity would inevitably lead to a supply glut, causing prices to crash. Profits would evaporate, and weaker players would go bankrupt or be acquired.

This boom-and-bust cycle created a deep-seated perception in financial markets. Memory makers have been seen tied to the volatile spot price of their chips, not to long-term technological leadership. It did not matter that only a handful of companies in the world could manufacture these technological marvels. The market saw them as interchangeable suppliers of a bulk product, like wheat or oil.

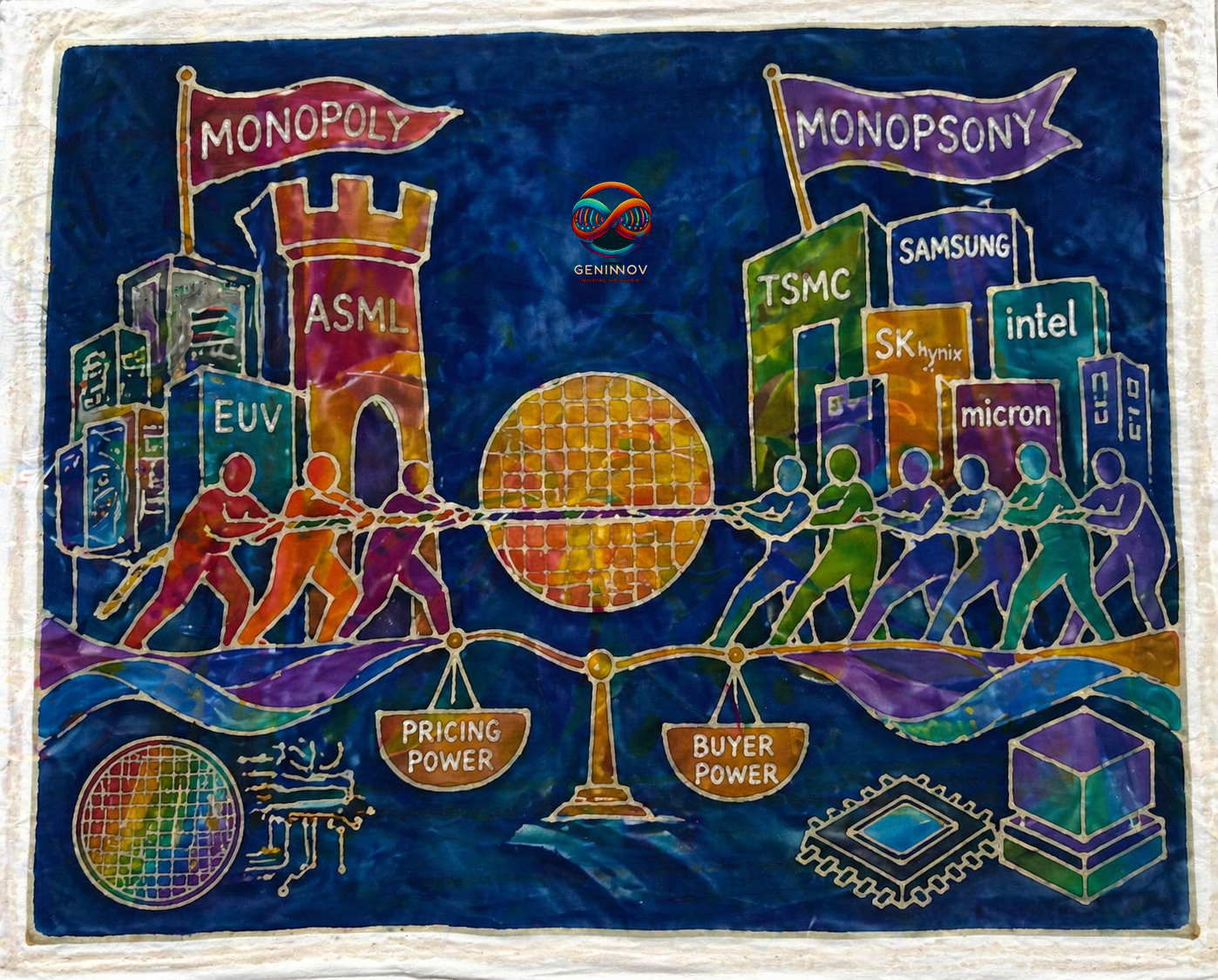

In short, it has been possible to hold on to this view and ignore the simple opposing truth: “Very few companies in the world can actually make modern DRAM or NAND at scale.” If memory makers have finally turned rational, it could be a tiny cartel with unusually high barriers to entry. The group is tiny in the cutting-edge variants like HBM, where only three players globally are viable, and one with an astounding lead. The “commodity” tag has overstayed its relevance.

From Commodity to King: NVIDIA’s Playbook

One swallow does not make summer. The reason behind the pricing power is in these companies’ drivers of non-off-the-shelf products. To understand their chart, let’s first trace NVIDIA’s history.

Not long ago, NVIDIA shared a similar fate. The company was primarily known for its GeForce graphics cards, a product line that lived and died by the consumer PC market. Its chips were, in many ways, high-tech commodities. They were sold off the shelf in electronics markets from Hong Kong to California. Gamers and PC builders would compare prices and benchmarks, and the cheapest card that met their needs would often win.

NVIDIA’s business was cyclical, its brand was strong but not unassailable, and its valuation reflected this reality. The turning point came when NVIDIA realized its graphics processing units (GPUs) had a hidden talent. Their parallel processing architecture was exceptionally good at the complex mathematics required for scientific computing and, eventually, artificial intelligence.

This discovery sparked a strategic pivot that would redefine the company. NVIDIA began to focus on the data center. Its new customers were hyperscale cloud providers like Amazon, Google, and Microsoft. These were not off-the-shelf sales. They were multi-million-dollar deals negotiated through deep engineering collaboration. This shift fundamentally transformed NVIDIA’s business profile.

Hynix's Ascent: A New Business Model

The winds of change that lifted NVIDIA are now blowing through the memory industry, and SK Hynix is at the center of the storm. The company is undergoing an NVIDIA-like transition, something that can be said about only a handful of companies in the technology sector over the decades.

HBM is not just faster DRAM. It is a completely different architecture. It involves stacking multiple layers of memory chips vertically, like a skyscraper, and connecting them with thousands of microscopic channels called Through-Silicon Vias (TSVs). This design creates a superhighway for data, allowing it to move between the memory and a processor at speeds that are impossible for traditional chips. This massive bandwidth is absolutely essential for feeding the data-hungry AI accelerators, like NVIDIA’s GPUs, that power modern artificial intelligence.

SK Hynix is the undisputed leader in this technology. Its mastery of the complex manufacturing process, particularly its proprietary Mass-Reflow Molded Underfill (MR-MUF) packaging technique, gives it a significant edge in heat dissipation and production yield. Competitors like Samsung and Micron have struggled to match Hynix’s quality and volume, facing delays and thermal issues. Their struggles are akin to those of NVIDIA’s competitors in the past.

Crucially, this has led to the creation of an entirely new business model. HBM is not sold on the open market. It is co-designed and co-developed with customers like NVIDIA. Sales are governed by long-term, negotiated contracts, which insulate this revenue stream from the price fluctuations of the commodity market. Hynix is no longer just a component supplier; it has become an integrated solutions partner. This shift is dramatically altering its revenue profile. The stable, high-margin, non-cyclical HBM business is rapidly growing, while the legacy commodity business shrinks. This is NVIDIA’s playbook, executed in a different corner of the semiconductor world.

Hynix: Tech’s Most Unrecognized Monopoly

Within the semiconductor industry, certain companies have achieved near-monopolistic control over their respective domains. Their dominance is widely recognized and richly rewarded by investors. ASML is the sole supplier of the EUV lithography machines needed to make advanced chips. TSMC is the undisputed leader in contract chip manufacturing. NVIDIA, well, we all know. Silly as it may sound for those not following the subsegments, but Hynix is reaching the standards set by these names.

While its dominance in HBM may not be as absolute as ASML’s in EUV, its leadership is formidable and its product is just as indispensable for the AI build-out. At this moment, if you are building a state-of-the-art AI data center, you are almost certainly using memory chips from SK Hynix. The company’s entire production of this critical component is sold out for at least the next 18 months, with pricing and volume locked in through negotiated contracts.

Its growth rates are more stunning than any of the others. Revenues have grown at triple-digit percentages in the last two years and are forecast to grow over 60% this year. Its profit margins are expanding, and the low-margin commodity portion of its business is in managed decline. It has a deep technological moat and a locked-in customer base.

Yet, remarkably, the company trades at a mid-single-digit price-to-earnings (P/E) multiple. This is not a typo. While other technology leaders with far less certain growth prospects command valuations of 30, 50, or even 100 times their earnings, the market values SK Hynix as if it were still stuck in the commodity bust cycle of a bygone era. The disconnect between its operational reality and its market valuation is staggering.

History, the Likes of Hynix, cannot Shake Off

Some things in the stock market simply do not make sense. Analysts and investors tie themselves in knots, building complex models to justify why a company at the heart of the greatest technology boom in a generation should be valued at a fraction of its peers. They will point to its history, to the ghosts of cycles past, to justify a P/E ratio of seven or nine.

Meanwhile, these same market participants will happily pay 25 or 30 times earnings for shares in the suppliers that sell materials and equipment to SK Hynix. They will pay even higher multiples for the customers who depend on Hynix’s technology to power their own growth. Everyone in the value chain, it seems, is allowed to benefit from Hynix’s success, except for Hynix itself.

Here stands a company that has fundamentally changed the nature of its business. It has escaped the commodity trap and established a dominant, high-margin position in a critical growth market. It boasts staggering revenue growth and a sold-out order book. Yet, it is continuously tormented by its valuation history. It is a fascinating absurdity. And it is a punchline hiding in plain sight.