For a quarter-century, the price of computer software and accessories fell by roughly 5% annually. It was the modern economy's most reliable disinflationary anchor. In late 2025, that anchor snapped. Last week, a technical note by three Federal Reserve economists, including a serving Governor until the day before the note's publication, revealed that this category just posted a 73% annualized spike over four months. Its contribution to core inflation? Nine standard deviations above the historical mean. A 1.2% sliver of the basket was adding roughly two-thirds of a percentage point to the Fed’s preferred gauge. The authors were careful, but their caution is the real charge. A quarter to well over half of the contribution may be measurement error: flash-memory prices leaking into a software index; CPI and PCE baskets that no longer match; subscription software and AI upgrades that old matched-model methods cannot see. The old disinflationary line has not merely turned. It has lost definition. The index is no longer cleanly measuring software. It is measuring a collision between memory, billing architecture, unpriced AI quality, and statistical plumbing. That is not a footnote to the inflation story. It is the story.

Halfway across the world, this exact force is violently reshaping current accounts. Japan, the nation that taught the world how to export electronics, just posted a record 7 trillion-yen digital deficit for fiscal 2024, tripling over a decade. It now bleeds over 10 trillion yen annually to foreign cloud and AI platforms, backed by a meager 4 trillion in digital exports. The Trade Ministry projects this gap will hit 18 trillion yen by 2035. In their worst-case scenario, it hits 28 trillion yen, eclipsing Japan’s entire oil and gas import bill. The country that once sold the world its technology now rents it back, and the premium is engineered to rival the cost of fossil fuels.

These are not two stories. They are one shock, seen through two accounting systems. Technology, which economists trained themselves to file under productivity, progress, and deflation, is starting to behave like energy: a strategic input, a price shock, a balance-of-payments channel, a geopolitical exposure. We call the investment-side expression Silicon Shock. But no one needs to use the term or own a chip stock to be exposed to it. Own a currency. Price a bond. Forecast a central bank. Manage a current account. Think about industrial sovereignty. The shock is already in the plumbing.

For half a century, the global economy's most critical chokepoint was the Strait of Hormuz. Energy was the price that mattered most. Today, that map is obsolete. Today's bottlenecks are not just physical straits and pipelines; they are memory packaging lines in Gyeonggi, logic fabs in Hsinchu, opaque cloud regions, and software billing gateways. These new chokepoints do not flash on petrol station signs, nor do they offer politicians an easy villain or markets a clean ticker. Their frictionless, invisible nature is precisely what makes them so dangerous. Macroeconomists may continually rework their models to argue that technology suppresses inflation, but the reality is the exact opposite. Through compute shrinkflation, capacity dilution, time dilation, and tiered API access, technology platforms are extracting significantly more capital for the same or less utility. Traditional inflation indices are entirely unequipped to capture this stealth pricing power. Yet these measurement failures must not obscure the fundamental structural shift: AI is an inherently expensive, highly inflationary technology, regardless of how long it takes legacy policymakers to realize it.

The Invisible Six Trillion Dollar Segment

Size is where this shift must be anchored, precisely because it is the variable most easily waved away. The legacy intuition assumes energy is the heavy, serious geopolitical input, while technology remains a consumer category adjacent to entertainment. That framing is now obsolete by a wide margin.

According to Gartner, the world will spend $6.31 trillion on information technology in 2026, compounding at 13.5% in a single year. Compare this to the physical world. The International Energy Agency expects total global investment across all energy sectors (oil, gas, coal, nuclear, renewables, grids, and storage) to reach roughly $3.4 trillion. Within that total, less than $500 billion is allocated to oil supply, marking a third consecutive year of decline.

The line that should stop the reader is artificial intelligence alone. Gartner puts worldwide AI spending in 2026 at about $2.5 trillion, up roughly 44%. AI, one subcategory of technology barely visible in national accounts a decade ago, is now being built out at a scale comparable to the entire global clean-energy investment machine and several times larger than annual oil-supply investment. The old hierarchy has inverted. For fifty years, energy was the input technology depended on. Now, technology is becoming one of the forces deciding how energy itself gets built.

The necessary caveat for the hostile reader is that IT spending represents a broad market aggregate, whereas the IEA figure measures capital investment. The caveat matters, but it does not rescue the old worldview. This is not an accounting identity. It is a map of economic attention. Technology compounds at double-digit rates; oil investment shrinks; data centers call for power plants; memory prices drive device cycles; cloud bills enter current accounts; AI capex changes electricity forecasts. Even if one refuses to crown technology as the single largest input in the world economy, the weaker claim is already enormous: technology has become one of the largest, fastest-growing, and least-observed macro inputs on earth.

The Bill That Arrives in Twelve Envelopes

Scale at the level of the world economy is one thing. The more telling place to look is the household, because that is where the invisibility turns almost comic. We will use US data to illustrate this dynamic, as it remains the most comprehensive and readily available. However, the structural arguments hold true globally, albeit with different absolute numbers and scales.

Energy, for all its political weight, is a shrinking share of the consumer wallet. The American Petroleum Institute, using official data, puts US consumer spending on all energy combined at about 5.7% of disposable income in 2024. That is down from 10% in 1984 and represents the lowest level in at least four decades. The Energy Information Administration has gasoline alone below 2% of disposable income in 2025, the lowest since 2005. The thing politicians fear most is, by share of income, near a generational low.

Now, try to add the technology bill. The phone plan. The home broadband line. Cloud storage. Streaming. Gaming. Security. Productivity software. App subscriptions. Device insurance. The amortized phone, laptop, tablet, and watch. And all of these arrive before factoring in the AI subscriptions that are rapidly becoming the single biggest household software expense. Deloitte's most recent Connected Consumer survey found US households spent an average of $896 on connected devices in 2025, up 17% in a single year, plus $183 a month on digital services. That is roughly $3,100 a year. It already covers the gasoline bill of about $2,150, even before accounting for software inflation and the backend metering that the survey fails to capture. The exact all-in figure is genuinely hard to state, and that difficulty is the point, not a footnote. No statistical agency publishes a fully loaded household technology bill. The absence is itself evidence.

Energy arrives as one large, salient line item that lands on the same day every month, which is exactly why it provokes. Technology arrives as a dozen small bills on a dozen different dates, none individually large enough to make anyone angry. A household paying $400 a month across eight technology line items feels nothing. The same household paying $200 once at the pump feels robbed. The dispersion is the disguise.

The poor-world version is sharper, because there the phone is not a convenience. It is infrastructure. GSMA estimates that more than 3 billion people already live within mobile-broadband coverage and still remain offline; coverage is no longer the binding constraint, affordability is. For much of the developing world, the handset is the bank branch, the classroom, the shopfront, the job board, the remittance rail, and the state portal. GSMA says even a $30 smartphone could bring 1.6 billion more people online. That tells you how close the margin is.

Now connect that razor-thin margin to the hardware squeeze. The rising cost of memory is systematically making $30 budget phones and sub-$500 PCs obsolete, pricing the cheapest devices out of existence. The true macroeconomic impact of this might only be felt years later, as the entry ticket to the digital economy silently slips out of reach for hundreds of millions. As we explored in our recent work on token inequality, physical constraints on semiconductor supply will dictate who gets access to the future and who gets locked out.

That is why technology inflation is regressive in a different and colder way than oil. Oil makes transport and heat more expensive. Technology can decide whether you enter the economy at all. It prices the poorest away from the most important productive asset they may ever own, at exactly the moment that asset becomes mandatory.

The Forty-Year Free Lunch

AI is systematically rendering multi-decade trends obsolete, which is precisely why we maintain that history is the worst possible guide for the AI era. Consider the casualties. The software layer is no longer capturing the lion's share of economic value. Technology has lost its privileged status as a sector where companies could expect to print money without heavy capital expenditure. But the most profound trend to break is a macroeconomic one: technology has lost its deflationary privilege.

To understand why nobody is prepared for this shift, you have to understand the belief that formed during the long, quiet decades when technology only ever fell in price.

For most of the past forty years, the information-technology line in the consumer price index ran negative year on year. Computers and phones got better and cheaper simultaneously, and the statisticians, doing their job correctly, recorded that as deflation. Technology was the obliging member of the basket, the one line reliably pulling the headline number down. A central banker watching inflation had no reason to fear a category that was helping. The instinct that formed was not neutral. It was affectionate. That affection hardened into doctrine, eventually codified as the Amazon effect, the idea that digital competition structurally suppressed prices. It became near-consensus that technology would always be disinflationary, as naturally as water flows downhill.

This is the time to introduce the reverse-symmetry argument. If a category falls by roughly 5% a year for decades, it is not neutral. It is a subsidy to the measured price level. It gives central banks room. It offsets pressure elsewhere. It teaches policymakers that technology is a friend. But when that same line stops falling, the tailwind disappears. When it rises, the tailwind becomes a headwind. One does not need an elaborate model to see the arithmetic. A force that subtracted from inflation for a generation no longer does.

The doctrine of ever-cheapening technology rested on two subsidies mistaken for laws of nature. The first was cheap physics. Moore's Law delivered more computing per dollar every cycle, making deflation look like an engineering inevitability. The second was cheap capital. The entire web era was financed by investors willing to subsidize growth, allowing services to be given away to capture users. Free became the default expectation for an enormous range of digital goods. More for less, forever, felt like a fundamental property of the technology. In reality, it was a property of the financing.

Both subsidies have expired, and they expired together. The physics got harder and, more critically, the wafers were rerouted toward a new and ravenous use case. The capital got expensive when rates rose, and the give-it-away model died with it. More importantly, and as we have written numerous times before, the entities at the world’s biggest chokepoints - we are talking about semiconductor manufacturers - realized the pricing power they have.

Effectively, technology has begun to behave like any other input. It costs what it costs.

Then came the use case that broke the pattern. Artificial intelligence is not Moore's Law. It does not get cheaper per unit of work the way a faster chip made an old task cheaper. Inference, the act of running a model, carries a real and recurring cost in compute and power that does not vanish with scale and, in many workloads, rises with use. AI is the first major technology in two generations that is fundamentally expensive and inflationary by its very nature.

This conclusion sits downstream of three arguments we have made previously. The cause is the Silicon Shock, highly concentrated and upstream. The mechanism is the tollbooth, defined by the metering and bundling in the middle. The consequence is token inequality, the per-unit economics that dictate who can afford intelligence and who is ultimately rationed. This inflation metric is where all three forces surface at once as a unified macroeconomic event.

A Dozen Disguises

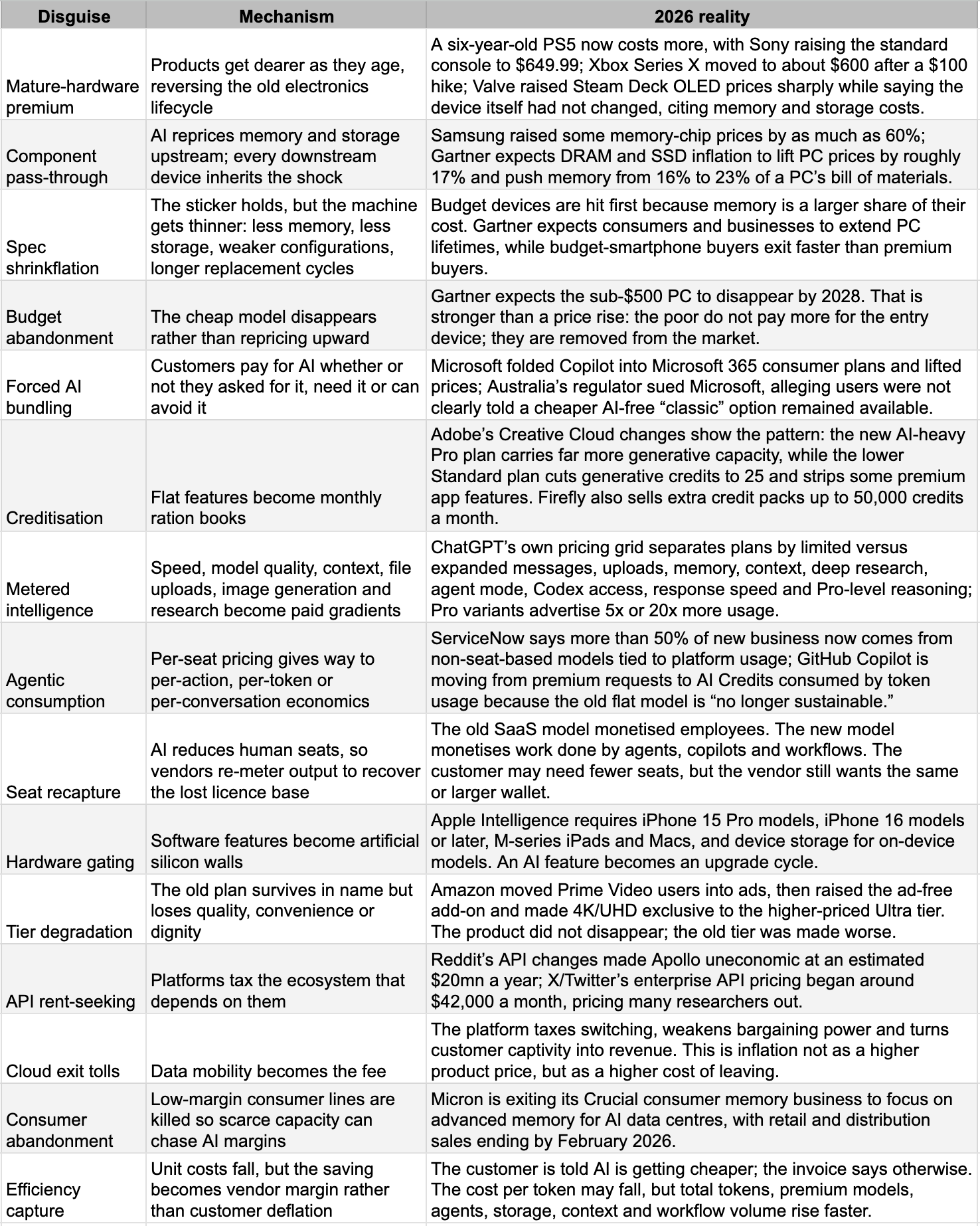

The mistake would be to hunt for this inflation where oil inflation appears, arriving as a single rising sticker. Technology inflation does not work that way. It arrives first where buyers are fragmented, bills are metered, and quality is hard to benchmark, which is precisely why it has stayed below the radar. It shows up as a mandatory AI bundle, a usage cap, a token meter, a thinner tier, or a degraded free plan long before it shows up as one clean price label in a shop.

Software inflation is not new. SaaS prices have outrun general inflation for years. What is new is not the number but the disguise. The Vertice index, tracking actual renewal prices across more than $30 billion in spend, has software inflation at 12% to 13%, about four and a half times the G7 rate and accelerating. Per-employee software spend reached roughly $9,100 by the end of 2025, surpassing employers' healthcare spending for the first time. But the headline rate only captures the prices honest enough to still appear as prices. Underneath, vendors fold in AI nobody asked for, convert flat features into exhaustible credits, and thin what each tier contains. Vertice found 28% of late-2025 renewals delivered less for the same money. An index can only count the dishonesty that still carries a price tag; the rest hides in shrinking value, and shrinking value never shows up in an inflation series.

The cleanest tell is the gap between cost and price. The raw input to AI collapsed: the cost of a million tokens fell roughly 280-fold in two years. Yet enterprise AI bills rose 320%, and software list prices climbed 12% to 15%. Some of that is genuine usage, but the list-price piece is rent, plain and simple. The efficiency gain did not reach the customer. It became a margin, if not for the model-makers then for the silicon bottleneck behind them.

The metering is starkest where intelligence is sold directly. Modelmakers are finding creative ways to charge for speed, priority, the newest model, and the number of questions you may ask. Intelligence is sold the way electricity is, by grade and quantity. The enterprise version runs on a harsher mechanism: AI is destroying the seat count software was priced on, because one augmented worker does the job of several, so vendors re-meter on consumption to recapture the lost seats. Salesforce launched its agents at $2 a conversation; a mid-size firm running 50,000 interactions a month now faces $100,000 a month on top of its seat fees, a line absent from last year's budget. GitHub is moving its coding assistant to usage billing because the flat model, in its own words, is no longer sustainable.

So software inflation is not merely a price increase. It is a mutation in the unit of sale. The old economy trained the customer to think in terms of seats and licenses. The AI economy trains the customer to think in rations: how many credits, which model, how much context, how fast, how many calls, how much to avoid the degraded version. A price rise says the same good costs more. This says something colder, that the good you thought you were buying is no longer the same good.

And it is not only new tech. For the entire history of the games console, hardware got cheaper as it aged. In 2026 a five-year-old PlayStation 5 costs more than at launch. The most dependable deflation curve in consumer electronics has inverted, which is the tell that this reaches everything, old and new.

This is why the official series keeps under-reading the shock. A statistics office sees a sticker price, not that the same laptop is a worse bargain because memory became unaffordable. It sees a subscription price, not the feature that became a credit, nor the AI bundle the customer cannot meaningfully decline, nor the tax of paying extra to strip ads from a product already bought.

The point is not that every firm is gouging. Some cost pressure is real: memory is scarce, inference is expensive, data centres need power. The macro question is who captures the efficiency gain and who pays the scarcity rent, and so far the answer is plain. The bottleneck takes the rent, the platform redesigns the bill, the customer gets the meter. That is why this is more dangerous than a normal price shock. Oil tells you when it hurts. Technology lets you discover it only at the renewal, the overage, the missing feature, the slower model, and the bill that somehow doubled without ever arriving in one place.

The Two Proofs

Arguments about hidden inflation can always be dismissed as mere complaints. So the case ends on two facts that are exceptionally hard to wave away, because they show the inflation biting the buyers best placed to escape it.

The first is that the richest corporations on earth have started rationing their AI consumption because it has become too expensive. Uber's chief technology officer disclosed that the company burned through its entire $3.4 billion AI budget for 2026 in just four months. Microsoft began canceling most of the internal licenses for the third-party coding assistant. A recent survey found 85% of companies missed their AI cost forecasts by more than 10%, and 84% saw gross margins fall by more than six points. Meanwhile, the share of corporate finance teams created specifically to police AI spending doubled in a single year. There is a profound economic point hiding in these anecdotes. These are the most price-insensitive buyers in the world. When even they start rationing, the price has cleared past what the entire demand curve will bear. You do not build a cost-control department around an input that is getting cheaper.

The second proof is subtler and, for a macro reader, far more damning. It is nominal growth on top of shrinking real volume, the textbook signature of inflation. TrendForce cut its 2026 notebook forecast from growth of 1.7% to a decline of 2.6% because rising memory costs are being passed into prices and choking demand. Yet revenue keeps climbing. HP shipped 4.9% fewer machines in a recent quarter, by Gartner's count, but still grew revenue. Its own chief executive blamed rising memory prices for the input-cost pressure. Fewer units, more dollars. The entire difference is price. This trend is not unique to one company: every volume growth number for technology gadget segments is in deep negative in recent months, while most of the major manufacturers continue to report healthy-growing top- and bottom-lines.

When a company sells less volume but books more revenue, that is not a growth story. It is inflation wearing a growth story's clothes, and it is now visible across the entire hardware industry.

The Fork in the World's Accounts

This is no longer only a story about prices. A bill rising this fast, on a good this essential, behaves like a terms-of-trade shock, the kind oil delivered in the 1970s. It moves money across borders, bends current accounts, pushes currencies, and reorders who is rich. Oil did it through one visible price. Silicon now does the same, less visibly, through a thousand invoices, and with a far shorter list of winners.

The winners are few enough to name in a breath. Korea's current account is heading toward 15% of GDP, of course, an all-time high. Taiwan's own statisticians have lifted 2026 growth to 9.64%, the fastest in a while. Both economies have the negatives from the ongoing oil shock, but the semi-gains dwarf any losses from the oil accounts.

The payers are everyone else, and the bill is starting to rival the one line every finance ministry already watches. China's largest single import is no longer oil. It is chips, and that too from 2024, before the current round of inflation. We discussed Japan’s plight at the beginning. And, these two are economies with large technology segments of their own.

In March 2026, Australia tipped into its first goods trade deficit since 2017, the single largest cause $2.9 billion surge in imported data-processing machines. Europe's apparent surplus is an Irish mirage, since 94 percent of the value booked in Dublin belongs to the foreign platforms routing the continent's revenue through it; strip that out, and Europe runs a structural deficit. The tech bill has quietly become a primary entry in the national accounts.

The United States is not exempt simply because it owns the platforms. Its software giants collect global rents, but its AI build-out imports astonishing amounts of physical infrastructure. A Minneapolis Fed analysis cited by the Wall Street Journal found AI-related imports surged 73% from 2023 to 2025, while non-AI imports rose only 3%; it estimated that without the AI-import surge, the 2025 US goods deficit could have been almost $200bn smaller.

The macro danger is that the silicon shock hits both sides of the balance of payments. The goods account pays for chips, servers, memory, and data-center equipment. The services account pays for cloud, software, model access, app stores, cybersecurity, enterprise subscriptions, and platform tolls. The income account then leaks profits, royalties, and licensing payments back to the firms that own the intellectual property. Oil was mostly a trade shock. Technology is a trade shock, a services shock, and an income shock at once.

That makes the currency channel nastier. A rising tech bill widens the external deficit. A wider external deficit weakens the currency. A weaker currency raises the local-currency cost of imported chips, cloud contracts, software licenses, devices, and energy. The country then imports inflation through the very exchange-rate move that was supposed to restore competitiveness. The adjustment does not stay politely inside “technology.” It leaks into every imported price.

It also changes the central-bank problem. If oil rises, a central bank can at least identify the shock. It knows the barrel price, the pass-through, the pump price, and the politics. With technology, the signal is fragmented. One part appears as hardware inflation. One part appears as software inflation. One part appears as a larger services deficit. One part appears as a capex import boom. One part appears as weaker real consumption because households are paying for more subscriptions and replacing devices less often. The central bank sees pieces of a shock and may mistake each one for noise.

The pressure is cumulative and accumulative, landing on a dozen different ledgers at once, and few showing signs of a reversion from falling demand. The winners, being few and highly content, have absolutely no reason to flag the imbalance. The payers, being many and each feeling the extraction individually across fragmented corporate and consumer bills, fail to raise a common alarm. The burden simply builds in the dark, effectively acting as an unvoted sovereign tax. That invisibility is exactly how the largest economic shocks invariably arrive.

Conclusion: The Oxymoron, and the Desk It Lands On

Until recently, the phrase "tech inflation" was a macroeconomic oxymoron. Technology was the engine that reliably made the future cheaper. That is precisely why the reversal is so dangerous. There is no instrument pointed at it, no political reflex trained on it, and no vocabulary ready to define it. For forty years, technology was the obliging friend, and you do not build alarms to watch a friend. Soon, this oxymoron will become a global preoccupation.

For a while, the establishment reflex will be to dismiss the data as a measurement error or an unsustainable cyclical blip. Macro analysts and policymakers are notoriously resistant to accepting a break from history until it becomes a monster in the rearview mirror. We saw this exact denial when government bond yields bottomed out a few years ago. Half a decade later, plenty of economists still mistakenly tether long-bond yields to stock market valuations. When market commentators get these novel forces wrong, they simply miss out on returns. When policymakers get them wrong, the societal costs are treacherous.

We maintain that the Silicon Shock is the defining economic event of this decade. Combined with the compounding force of AI, it will drive structural divergences that will be nearly impossible to reverse for those who arrive late. If the largest and richest corporations on earth are already feeling the pinch of AI costs, sovereign nations are inevitably hurting as well. The fact that so few have begun complaining in policy circles, regardless of whether they have solutions, perfectly illustrates the stealth, insidious nature of the shock.

And even seen clearly, the shock runs into a genuinely new bind. This has the profile of a supply shock from a concentrated foreign source, the same shape as oil, and central bankers have always refused to fight supply shocks with rates, which is why they strip food and energy out and watch core. By that logic, they should strip memory-driven tech inflation out, too. So here is the question nobody wants to answer out loud: should the cost of high-bandwidth memory be excluded from the core the way a barrel of oil is? The trouble is that you cannot strip out what you cannot isolate. Energy is one clean line you can lift from the index. Technology is smeared across devices, software, services, and the quality adjustments buried inside dozens of other categories, with no clean line to remove. And the rate lever barely reaches it because the capex doing the pushing sits on hyperscaler balance sheets that higher rates do little to slow, while costs land now and productivity, if it comes, lands later. A supply shock with the volatility of energy, the persistence of services, the reach of nothing they have excluded before, and a tool that does not quite touch it. That is the desk it lands on.

An uncomfortable aside belongs here, and it is worth stating plainly. For the companies at the centre of this bottleneck, falling volume matters strangely little because aggressive price hikes entirely subsume it. Their input costs rise, they pass the increase through, they add a margin on top, their unit shipments fall, and their profits still climb. It is neither ethically nor politically defensible to celebrate an industry that grows its earnings by selling less product at a higher price to a captive world. But it is the reality, and it explains why these equities keep climbing even as the underlying commodity becomes scarcer and dearer.

The world spent half a century learning to recognize an oil shock. It is now entering a technology shock with no equivalent dashboard, no political vocabulary, and no accepted policy reflex. The danger is not merely that prices rise. It is that the gains accrue to a localized handful, the costs travel diffusely, and the watchmen are still staring at the oil markets.

The next great macroeconomic shock does not arrive in a barrel. It arrives in a server rack, in a degraded specification, in a metered token, and in a current-account balance bending under the weight of imported silicon. Technology is no longer just a tool sitting inside the economy. It has quietly become the price-setting infrastructure of the economy itself, and we are about to spend a long time learning exactly what that costs.