The accepted wisdom in GenAI model making is that the door has closed. To build at the frontier, as per perceptions, is only for those who began years ago, with a real lab, a research culture compounded over time, and a head start that no cheque buys back. The train seems to have left the station for someone with ambitions but without a start.

Xiaomi provides more than an encouraging counterexample. This is a story of a model called MiMo that should have been used as bait, with many surprising achievements, whose company name was only revealed later. Unfortunately, we have to ensure our titles and bylines specify enough for readers to decide whether to open the mail. So the surprise this story deserves is the one I am not allowed to spring. Hold the name and forget it at once, because for a few weeks earlier this year nobody knew it, and the not-knowing is the proof.

In March, a model appeared on a developer platform under a codename, with no maker attached. It climbed to the top of the usage charts and passed 1 trillion tokens served before anyone could place it. The community reached the only conclusion its map allowed, that this had to be the unreleased DeepSeek, because the alternatives were unthinkable. It was not DeepSeek. It was from Xiaomi, of course, from a company most investors file under phones, rice cookers and the occasional electric cars.

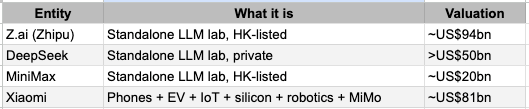

The timing makes it a parable. This is a week when markets, in Hong Kong and China as much as in the US, are again arguing over what a model is worth, pitting the valuations of labs that make nothing else against those of companies that make everything else. Xiaomi now has lesser market capitalization than Zhipu AI, which would not be a discussion-worthy consideration ordinarily given what is going on in the US. Except that Xiaomi, with tens of times the revenue and remarkable innovation across several fields, also owns a model that on many counts is more exciting than the listed pure-plays it is being measured against.

Once again, the people who should read on are not only Xiaomi's shareholders. They are everyone now drafting a national or corporate model on the assumption that it takes a decade, a fortune and a ten-year head start.

The Price of Building LLM Within a Corporate Setup

The Standing Start

Almost every serious popular GenAI model carries a version one dated 2023 or earlier. This is as true of ChatGPT and Claude as of Mistral, DeepSeek or Qwen. To someone embarking on a generative model today, it would appear that the whole board was set before 2025 began.

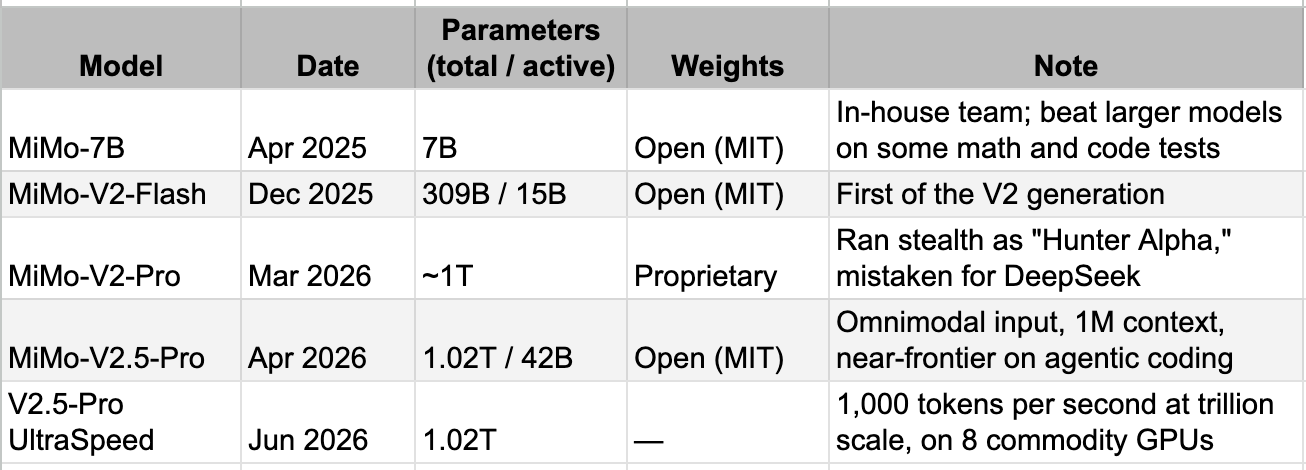

Xiaomi's first artifact, a 7-billion-parameter reasoning model built in-house, arrived on 30 April 2025, deliberately small and tuned to punch above its size on math and code. That is the entire starting line, and it was barely a year ago.

Some will say Xiaomi had not arrived from nowhere. It had run a voice assistant, Xiao Ai, since 2017, but that was AI in name only against what gets counted as AI now. On paper it built a large-model team inside its AI Lab in early 2023 and shipped its first language models, the MiLM series, that same year. But those were tiny by design, built for the edge. Effectively, Xiaomi had nothing that could stand against even the lowest-ranked frontier model until last year. The version-2 tags on the MiMo series tell the same story. What the table below tells is the more important part, that the rise in the series has been nothing short of staggering.

From a 7-billion-parameter start, the company had a 309-billion-parameter model in eight months, and in eleven a trillion-parameter one good enough to be mistaken for the most anticipated model in China. Inside a year the model turned multimodal, went open-source, and now lands consistently in the middle of the major ranking tables, more often than not ahead of models from companies carrying market capitalization higher than Xiaomi.

The part the market has not absorbed is that almost none of the advantage has been collected yet. A reputation in models is built slowly, by developers who try a thing, trust it, and tell others, and Xiaomi has only just given them something to trust. An ecosystem forms the same way, as adapters, fine-tunes, deployment tooling, and integrations accumulate around weights that people have decided are worth building on, and that accumulation began months ago, not years. These are assets that compound. Each capable release lowers the cost of the next, each developer who adopts the model makes it likelier the next one will, and each device the model touches returns data that sharpens it. Xiaomi has spent the year laying the first courses of that foundation. The structure it is meant to support is still mostly above ground level, only on paper.

As impressive as the catch-up has been, the more interesting claim is that there should be more to come. Late in 2025, Xiaomi brought in a senior researcher who had helped build DeepSeek's own models to lead the effort. The inflection in the table lines up with the arrival of her and her team, and the honest read is not that they have peaked but that they have barely started.

MiMo Leading the Price League Tables

The early model was, by the honest accounts of the people who used it, verbose and prone to wandering, with the math slips and the bloated token counts that betray a young model trying too hard. A year later those are mostly gone. Independent measurement now rates the flagship as concise rather than chatty, and places it on the efficiency frontier, hitting comparable quality at materially lower token counts than its peers. On the dimension that matters most for agentic work, staying faithful to instructions across very long runs, it holds together over sessions of thousands of tool calls without losing the thread. Xiaomi's own demonstrations include a compiler written autonomously over several hours and passing every hidden test, the kind of run that is impossible if the model is drifting. The context holding is so strong that readers may come across an article in which the model is said to be “superior to Claude Code.” To be fair, that’s valid in an extremely limited context, but it does not invalidate the point that this young model is rising extremely rapidly.

Technically, MiMo-V2.5-Pro is a trillion-parameter mixture of experts that runs natively across text, image and video, with a one-million-token context as standard, and it was first among the world's open-source models on the main intelligence index at launch (it is no longer). Its ability to hold threads, discussed in the previous paragraph, is the property that separates a model you can deploy from one you can only demo. And here is the tell. Xiaomi launched the V2 flagship as a closed, proprietary product, then turned around and released V2.5 under an MIT license, weights in the open, free to modify and ship commercially. This is the flex on one’s confidence in the product: you do not give away what you are unsure of. Open-sourcing the better model is a confidence signal written in source code.

On raw capability, the model is not close to the ones at the frontier. It is below the closed leaders by a clear margin on the broad composite, but likely ahead of Mistral, ahead of Meta's open line, behind Meta's new closed model and behind xAI's flagship on many benchmarks and parameters. On a two-to-three-month average rather than a launch-week peak, it sits in the top tier of Chinese coding models without being the leader of it, with Kimi and GLM ahead on the hardest agentic benchmarks and DeepSeek the more consistent daily driver. What it wins, and wins decisively, is value. It carries near-leading coding scores at roughly a fifth of the price of the Western frontier, under a fully permissive license, with fewer tokens burned per unit of work.

MiMo’s clinching number is economic. One autonomous run chewed through 387 million tokens for about 70 dollars, because a 96 percent cache-hit rate turned repeated context nearly free. Developers may not be admiring the benchmarks. They are voting with their tokens. In late May it cut the MiMo card by as much as 99 percent and scrapped the surcharge for long context, so a million-token call costs the same as a short one. The new card is not merely cheap. It is, to the decimal, DeepSeek's card. Both charge 0.025 yuan for cached input, 3 for uncached, and 6 for output, and Xiaomi's cut runs directly against Zhipu, which raised its prices instead. That mirroring is deliberate, and it is selective. While Xiaomi and DeepSeek cut toward zero, Zhipu lifted prices 83 percent and Alibaba and ByteDance quietly pulled their cheapest tiers.

In the week when Microsoft is rumored to be weighing DeepSeek as an option for CoPilot Cowork as a low cost option, it is worth pausing to consider Xiaomi's choice. Generally, a model a few months old normally charges what it can while the capability is fresh, to recoup the training bill or to ration scarce capacity. Xiaomi did the opposite, pricing a new product for habit and mind share before it has earned a yuan, which is the move of a company sure of what it built and surer of how it wins. This is the hardware reflex transposed onto software. Take the user first, worry about the toll later, and let the ecosystem do the monetizing the model refuses to. The result is a contender that matches the lab the market just valued above 50 billion dollars on openness and on price, beats it on modality, and is pulling developers across in real time.

Has Xiaomi Got the Techflation Era Memo?

Now that Apple has announced it will raise prices, techflation is likely to become a viral global theme soon. We have repeatedly discussed, in multiple pieces, how AI is an inflationary, unequal, and expensive technology, and how even companies under other business pressures are raising prices without worrying about the impact on volume. Everyone seems to have gotten the memo except the company this essay is about. For all gadget-makers, the falling bill of materials had been a decades-long trend, which let the likes of Xiaomi hold prices, widen a margin, or cut a tag to take share, and usually some of all three. Memory was the most reliable part of that gift. It is now the most expensive surprise on the bill. The cost of the chips inside a phone has roughly doubled in a single quarter, and memory that was a single-digit slice of the build a year ago is approaching a fifth of it.

Xiaomi has repeatedly announced the possibility of imminent price increases since the second half of 2025, but its actions have not adequately matched its words so far. This is likely because its products sit where the inflation bites hardest, in the price-sensitive middle and bottom of the market, the exact place where a buyer who sees a higher number walks to the shelf beside it. So it has held and withheld. Holding the price was supposed to protect the volume, and it has not. Its handphone shipments fell about a fifth, the steepest drop of any large maker in the world, and the margin on what did sell still collapsed, because the cost came through regardless of whether the price moved. The stock has roughly halved over the year as this arithmetic became clear.

The car was meant to be the second engine and has become the second worry. Orders were never the constraint. The gap between promise and delivery was. The wait on the SUV stretched toward a year, long enough that the founder told impatient buyers to consider a Tesla. Safety did more damage to the premium story than any competitor. A fatal crash forced the recall of nearly 117,000 sedans over a driver-assistance flaw, and a fire in which the electronic doors would not open prompted a safety committee. The volume push toward more than half a million cars a year is bought with margin, and the division swung from the prior year's profit into the loss above.

The newest worry is particular to where these shares trade. Xiaomi is seen as a handset company, so its AI spending is not read the way a pure model maker's is. Its followers have decided it is spending too much, and the structure of that spending makes the fear self-fulfilling. The intelligence is given away by design, the API priced in a war that loses money on every call, the bill running to billions over the coming years and landing inside the loss-making division. This is the cruelty of the corporate wrapper, and it has hidden great assets before. Korean markets ignored the value of Boston Dynamics inside Hyundai Motor Group until early this year. Sum-of-the-parts arrives late at Asian conglomerates, and only once the innovation becomes impossible to ignore.

The case is coherent and not foolish. A phone maker losing share into a cost shock it will not pass on, tied to a car business buying volume with margin and an AI habit that consumes cash and returns none. Every figure in it is real. It holds together on a single assumption it never tests, that what sits inside the wrapper is only ever a cost.

The Integrator’s Edge

How many companies that are neither software houses nor model labs have built a competitive large language model in-house? Worldwide, the list rounds to one. Apple has spent more and delivered less, its assistant overhaul slipping by years. Samsung leaned on other firms' models and put its name on the output. Two companies with the deepest distribution on earth could not turn it into AI of their own. Xiaomi did, on a stack it controls down to the silicon, with its own 3nm processor sitting in the phone. The feat was never the research. It was the integration, which is the discipline the larger companies keep failing.

Management has put both a figure and a shape on the ambition, and neither is inference. R&D reached RMB33.1 billion in 2025, a record, taking the prior five years to RMB105.5 billion. The next five carry a pledged RMB200 billion, about $28 billion, close to double the last cycle, aimed sharply at chips, AI and operating systems. The rationale is stated, not hoped for. Lei Jun has framed 2026 as a "grand convergence," a self-developed chip, a self-developed operating system and a self-developed model meeting on a single device, in service of the "people, car, home" ecosystem. The three pieces already have names. The chip is XRING O1. The operating system is HyperOS, which already runs AI through its system applications, from writing and captioning to real-time translation and summaries. The model is MiMo. The plan is to fuse them, and the spend is the price of fusing them.

The way we read it, and this is not how the company has framed it, the model is given away by design rather than generosity. Xiaomi has no need to sell intelligence by the token, because it sells the devices the intelligence makes better. Open weights and a price cut to the bone buy habit and mindshare now, while the value that compounds is taken inside the product later.

That product path is the part a model company cannot copy, and the lever is multimodality. Hundreds of millions of phones, cars and homes generate image, video, audio and sensor data from the physical world, the kind no standalone lab can assemble at any price. The same model line that reads it is being pointed at the agentic layer, software that acts across the phone, the car and the home rather than only answers, and beyond that at the embodied work, where one vision-language line feeds both an in-car autonomy stack and a humanoid program. The flagship never has to run on an appliance. It has to make the small model that does run there better each cycle, and turning model quality into product on constrained hardware is the one thing Xiaomi has spent fifteen years learning to do.

The Case Against

A note this favorable owes the reader the bear on the idea, not just on the share price, and there is a real one.

Start with the capability. Much of the lead is self-reported, and the independent reproduction is still thin. The flagship trails the live frontier and slips further as the leaders pull away, and even within its own neighborhood it is not the front-runner. On a multi-month view rather than a launch-week peak, Kimi and GLM are ahead on the hardest agentic work, and DeepSeek is the steadier daily choice, and some heavy real-world agent loops come out cheaper on DeepSeek despite matching list prices, because cost in practice turns on cache behavior, not the sticker. The strongest claims for the model are the youngest, and youth is not yet a record. Given the recent releases, one may expect a quicker pace of announcements from Xiaomi and a continued recapture of leads in league tables and in user imagination, but nothing in model making is guaranteed. Plus, the Chinese model-making landscape is brutally competitive.

All the political, compute, and other risks associated with other Chinese models apply to Xiaomi. If we are wrong and Xiaomi continues its push to be a DeepSeek contender rather than focusing on building the model for applications within its ecosystem, there will be additional risks of failure and overspending.

The hardest objection is the one the bull case leans on. The Google parallel flatters because Google's surfaces monetized the model directly, on a profit-and-loss statement the market already trusted. Xiaomi's surfaces monetize it sideways, through stickier hardware first and new categories later, and that signal is tangled up with successes in other innovations, say in robotics hardware or cars. The asset may be every bit as good. The path from asset to printed earnings will not be just about the models.

None of this breaks the thesis in a market that has completely ignored these developments.

Conclusion: Premium or Discount for All Under One Roof?

Open Xiaomi in any news feed on any given week and the range is the story. A 3nm phone processor designed in-house, with the company now committed to a new one every year. A humanoid that has gone from stage prop to factory intern, tested on the line of Xiaomi's own car plant at a 90 percent success rate on autonomous assembly, the same plant that has now built its 500,000th vehicle. A frontier-class model. An operating system. Four new cars in a single year, alongside the wearables, the vacuums, the imaging. Xiaomi is one of the most prolific innovation engines on earth, and it is priced only for the phone business that is not doing well.

The breadth is not a scatter of hobbies. It is the mechanism. The model that reads a room trains the robot that works the factory that builds the car that returns the data that sharpens the model. The chip team that learned a node in a phone carries it into the car and the robot. The motor and battery work crosses from the vehicle to the humanoid. Expertise bought once in one product line ports to the next at almost no marginal cost, which is precisely the property that decides winners as computing leaves the screen and moves into the physical world. The integration is not the overhead on the innovation. It is the innovation.

That raises the question management cannot dodge, given where pure-plays trade. Why not surface the value the market will not see on its own. Hive off the model, where standalone labs fetch tens of billions. Hive off the cars, where a clean vehicle multiple would dwarf what the group is credited for them. The financial logic is real, and the market is rewarding exactly this surgery elsewhere this year. But it misreads the asset. What makes Xiaomi singular is not the model, the car, or the chip. It is that they live together and feed one another. Hive off the model and you have sold free weights with no earnings to carry. Hive off the cars and you have severed the factory teaching the robot. We, for one, would rather the company resist any temptation to split its assets. Its time is perhaps far better spent executing on its strategies.

As we have repeatedly discussed in these notes, amazing assets continue to get completely ignored in Asian marketplaces. Xiaomi, at current prices, has the potential to join the illustrious list. That said, its phone business may not simply be a neutral news provider, like Hyundai Motor’s core business was, for the value to be recognized in quick time.