The Sound of Silence

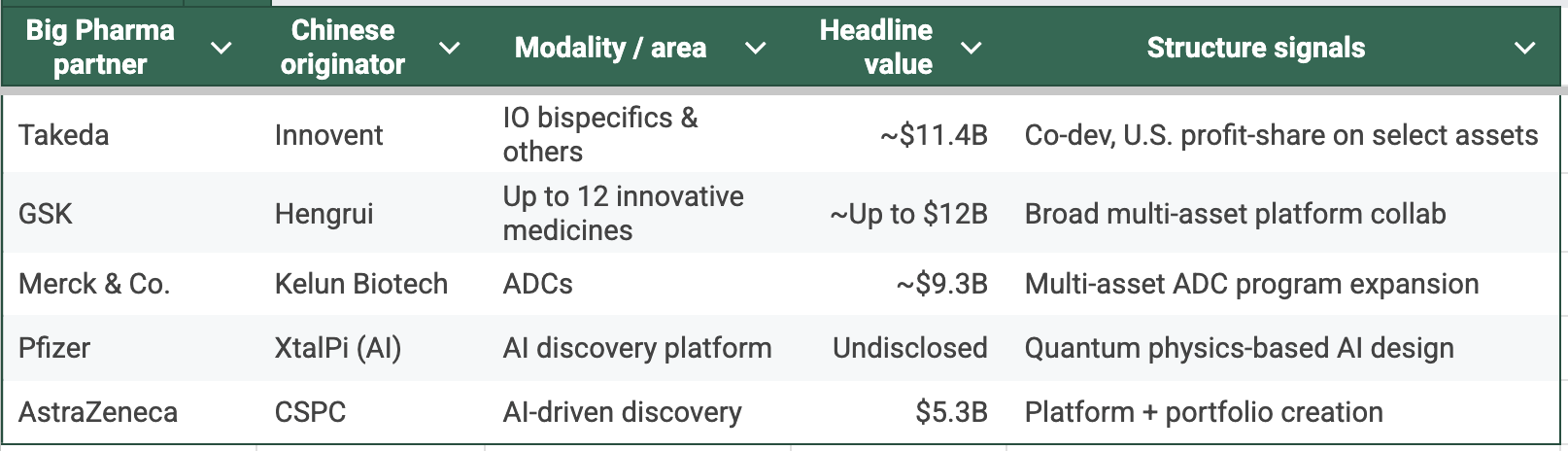

Recently, Innovent Biologics, a Chinese pharmaceutical firm, announced a deal with Takeda. The Japanese giant was paying $1.2 billion upfront, with a total potential value of $11.4 billion, for a handful of Innovent's cancer assets. In some ways, it is a deal that could redefine cancer care worldwide, featuring two late-stage powerhouses: IBI363, a bispecific antibody fusion protein targeting PD-1 and IL-2 for non-small cell lung and colorectal cancers, and IBI343, an ADC targeting Claudin 18.2 for gastric and pancreatic tumors. Takeda grabs global rights outside Greater China, planning U.S. manufacturing to dodge tariff headaches.

The market’s reaction to the deal that nobody anticipated? Absolutely nothing.

Days later, there was another quake. Innovent’s metabolic drug, mazdutide, went head-to-head against semaglutide, the active ingredient in the blockbusters Ozempic and Wegovy. In a Phase 3 trial, Innovent's drug was not just "non-inferior"; it was superior. In the key trial objective, 48% of patients on mazdutide achieved significant blood sugar and weight loss goals. Only 21% on semaglutide did.

Again, silence in stock prices. If Lilly had posted that against Novo, one share might have gone up by double digits on the day, and another down. Analysts would have produced volumes dissecting every number to examine the claims. TV panels would loop it for days.

This isn’t another “Asian innovations do not get properly noticed by markets” lament. It’s broader. This cognitive dissonance is not just about a single mispriced stock. It is a failure to see a fundamental, structural shift in the global order. For decades, the global pharma narrative has been written in Boston, Basel, or Tokyo. China was the factory, the trial site, the CDMO. Not the innovator. That assumption is now obsolete, and the implications are substantial

The Club That Wouldn’t Change

For more than three decades, the global pharmaceutical industry has been an exclusive club. We call it "Big Pharma." Its roster has stayed oddly static. Same geographies. Same names, re-arranged by M&A. The traits were textbook: tens of billions in revenue, dozens of late-stage programs across many therapeutic areas, end-to-end manufacturing and sales in every major market, R&D underwritten by cash cows. Barriers everywhere: capital, trials, regulation, distribution, policy. New companies arrived through acquisition, not by joining the club.

That stability wasn’t an accident. It was structure. Global regulatory know-how is hard to buy overnight. So is a field force across the U.S., EU, and Japan. So is a safety database that clears every Health Authority question. When midcaps broke through, they were typically folded in. The scoreboard changed through consolidation, not through new entrants.

Separately, China’s biopharma decade began at the periphery of that system. Contract research. Manufacturing. Biosimilars. Programs that could fund capability-building without demanding global brand muscle. The early verdict, unfair but common and still prevalent, was: great doers, not originators.

The Challengers Who Built Their Own Keys

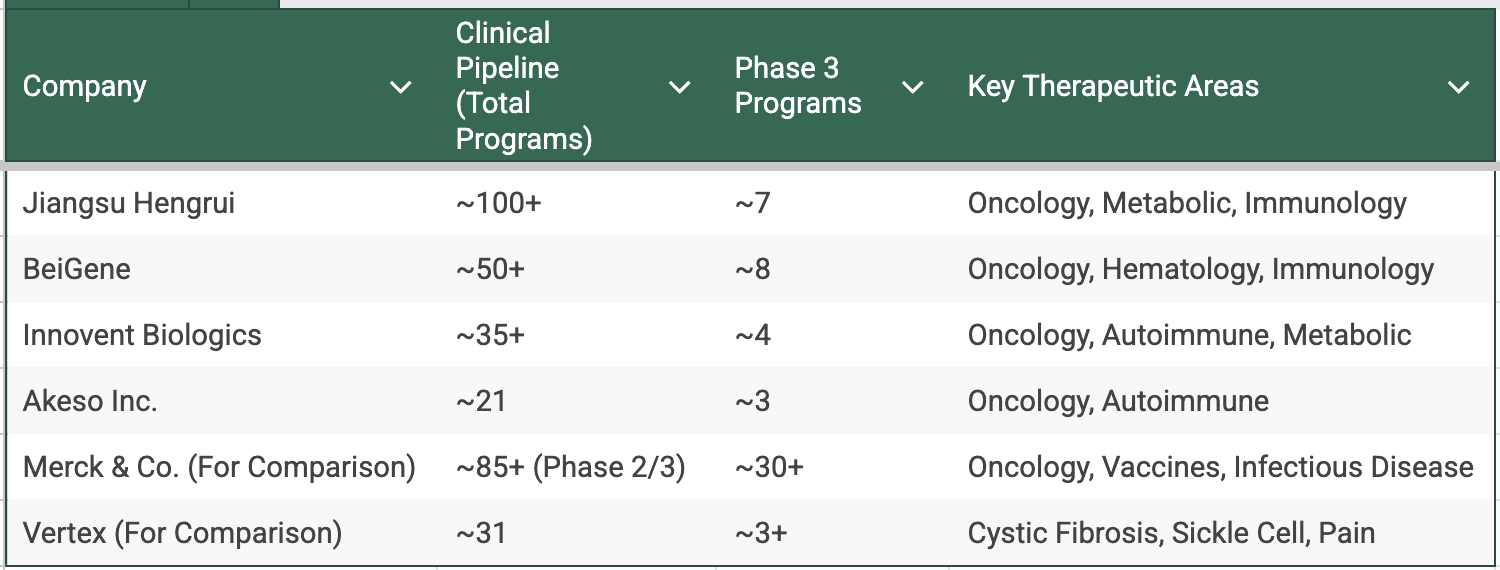

Over the last few years, China’s leaders went horizontal as they pioneered a novel and highly effective "biosimilar-to-innovator" strategy. Not single-asset punts. Multi-therapy portfolios. Oncology first, then metabolic, autoimmune, cardiovascular, even ophthalmology. The counts are startling to anyone stuck in the 2017 mental model. Hengrui with hundreds of active trials. BeiGene is running global registrational programs. Innovent stacking late-stage assets beyond oncology. Akeso is pioneering PD-1-based bispecifics and ticking off approvals. This is no longer “one molecule, one hope.” It looks like an engine.

Quantitatively, the results of this strategy are now undeniable. The pipelines of China’s top firms are not just deep; they are beginning to rival the Old Guard in scale and breadth.

Is the scale “Pfizer-class”? Not yet. But these are not "biotech" numbers. Jiangsu Hengrui is running over 400 clinical trials. BeiGene has over 170 trials active globally. These are "Big Pharma" numbers. The shape is Big-Pharma-like: diverse modality set, parallel late-stage bets, and financing models that don’t depend on one asset clearing every gate. That shape matters. It’s how you weather misses, and it’s how you credibly partner on equal terms.

From Biosimilars to Engines of Discovery

Two flywheels spun up the engine. First: cash-flow and know-how from biosimilars and contract work. That funded people, platforms, and plants. It also forced a discipline large pharmas respect: lot-to-lot consistency, scale manufacturing, global QA. Those muscles translate when you switch from copies to invention.

Second: regulatory reform. China’s NMPA accelerated reviews, opened priority pathways, and harmonized with ICH standards. That pushed assets through pre-clinical and early clinical faster, swelling the pool of genuine innovation. By 2024 the count of novel approvals hit records.

Deal flow told the same story. 2024–25 saw out-licensing values that would have been unthinkable in 2019. In the first half of 2025 alone, out-licensing deals from Chinese biotechs accounted for 44.5% of the global total in deal value. These are not just “tolling” deals. Profit-share, co-dev, co-commercialization. Western buyers are not merely renting capacity; they’re renting growth.

But there is a second, far more ambitious strategy. It is the "Global-from-Day-One" approach. The prime example is BeiGene. With its BTK inhibitor, Brukinsa, the company did not seek a Western partner. It ran its own global, head-to-head clinical trials against the multi-billion-dollar incumbent from Johnson & Johnson. It proved superiority in both efficacy and safety to receive an FDA approval. It went on to build its own commercial sales force in the United States and Europe to launch the drug independently.

Are these one-off examples? Skepticism is healthy. One trial doesn’t rewrite guidance. Head-to-heads need replication. Safety must mature over time. Global filing packages must pass FDA and EMA scrutiny, not just NMPA. All true. But the prior belief that a Chinese originator could not lead in the hottest global category has been failing live tests.

Deals in Recent Years

No Legacy. New Tools. Faster Loops

Legacy's the ball and chain Big Pharma can't shake. Patents? A minefield. Keytruda's 2028 cliff: $200 billion void. Humira's bioswarm: sales cratered. Chem-pharma roots? Rigid, slow to biologics or AI pivots. Clinical trials cost $69K per patient in the U.S., versus $25K in China. Enrollment that takes a year in Europe can wrap in months in Shanghai. Protecting relics? Billions diverted with evergreening tweaks cost $1-2 billion per drug. Pfizer CEO Bourla captured it succinctly about a fortnight ago: "In biopharma, China's dramatic speed, cost and scale have triggered a shift in the global competitive landscape.”

Chinese challengers started on a blank page. They did not have to worry when disruptive forces arrived. Cloud first. API-first data. Single-tenant labs built around automation from day one. AI isn’t a thing to bolt on; it’s in the wiring. Closed-loop robotic labs are not slide shows; they exist in Suzhou, running discovery cycles that compress months into weeks.

The ecosystem multiplies it. Tech giants — Tencent, Baidu, Alibaba — built healthcare AI stacks. Because of the cutting-edge CDMOs and the ecoscape they create, a molecule can go from concept to IND in 12–15 months, half the global average. Startups like Insilico and XtalPi ship tools that pharma can actually use. Patent output in AI drug discovery exploded, providing a rough proxy for effort (by some counts, over 38000, they are six times those of the next nation on the table). Meanwhile, government policy named AI+biopharma a formal priority.

In one line, Big Pharma is retrofitting AI into century-old structures. Chinese biotechs were born digital.

An Innovation Trend Not Going Away

One can write a far longer piece on the caveats. In fact, one sees them all the time in write-ups on the US Biosecure Act, in data trusts, in privacy concerns, in export controls, in FDA and other regulators’ higher standards, and in many other standard factors.

The reality is that the global patent cliff between 2025 and 2030 is the biggest in memory. Hundreds of billions of revenue at risk. For “Big Pharma,” replacing that with internal R&D alone is unrealistic. Portfolio chiefs are raiding the world for credible late-stage assets. China’s pipeline finally had enough of them to matter.

This brings us back to Innovent. Back to the silence that met its $11.4 billion Takeda deal and its clinical victory over Ozempic. Maybe this is a one-off. Fully justifiable in the way we do not see yet, but markets will surely make us learn if wrong.

What is certain is that the era of immutable pharma hierarchy is over. The club is no longer static. It’s expanding, and the new members are rewriting the playbook. Irrespective of stock market habits and ways of assessing things, we all need to pause to consider the impact of the most significant structural shift in the pharmaceutical world in a generation.